Mind the gap

Why timing differences can skew short-term relative performance figures

Like most open-ended investment funds (OEICs), our range of funds has a ‘valuation point’ of 12 noon each day. What this means is that the prices are taken of the assets held at 12 o’clock on that day and used to determine the price of our Adventurous, Balanced, Cautious or Global Equity portfolios.

Real time

For some of the holdings, this is easy. For our holding in exchange-traded funds (ETF) like the FTSE 100 Index ETF or defined returns products such as the Goldman Sachs Autocall, for example, it’s just a matter of looking at what the price on the screen is at that time and using that for the calculations.

Yesterday

However, the majority of holdings in our funds are other funds, many of which at 12 noon are still at the price determined at midday (or 10am) on the previous day. Thus, for our OEIC price today we have to use the price of the funds yesterday which builds in a time lag.

Or even the day before

A few funds we hold are valued at close of business. This can add another lag depending when the price is published, because sometimes these are not available in time for our 12 noon valuation. In this case the values from the close of business two days ago are used for calculating our prices.

What does this mean?

Whilst this is a technical pricing matter (it does not alter the value of clients’ assets) it is worth bearing in mind when looking at short-term performance numbers.

We often compare our fund returns, for instance, against those of the FTSE 100 Index. The Index values the top 100 companies at 4:30pm every working day but clearly this can be very different from the prices used for our funds given we value at 12 noon and the time lags in pricing we have talked about.

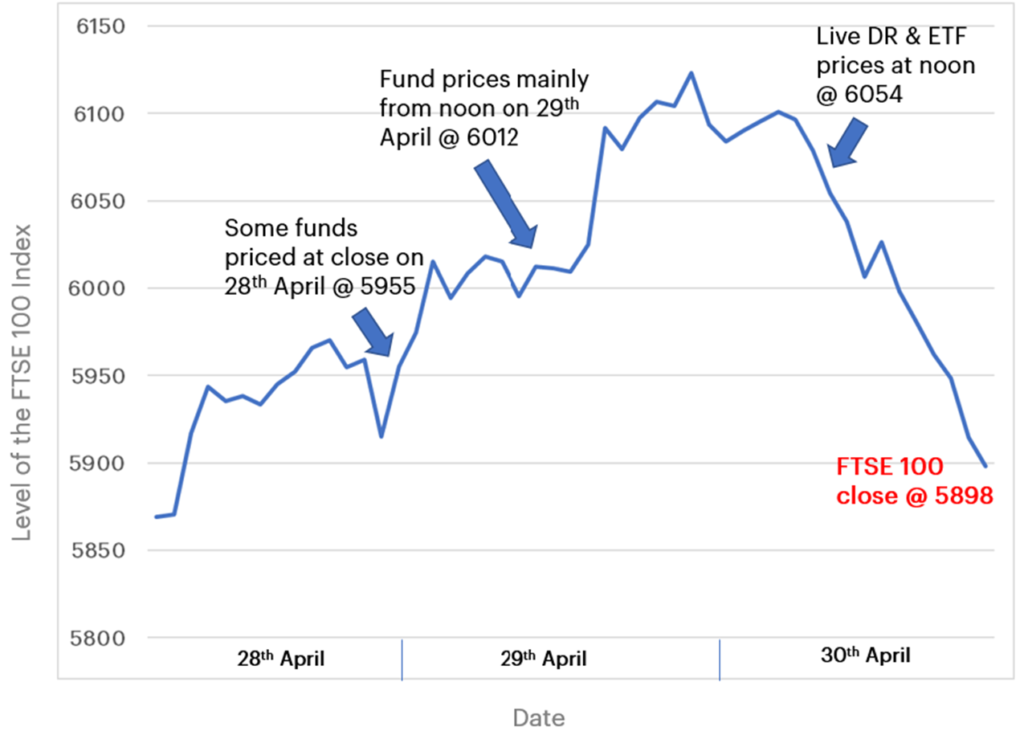

If we take the example of the last day of April this year, we can see what a difference there is between the 12 noon level of the market and that at the close of business:

30th April 2020 – FTSE 100 Index

12 noon: 6054

Close: 5898

% change: -2.59%

So, even if there were no lags in valuations, comparing our funds against the FTSE 100 Index would make them appear to have nearly 2.6% better performance because the Index fell in the afternoon.

If we then added in the effect of the lags, this would alter the valuations further, as illustrated in chart one below:

Chart one – FTSE 100 Index price index 28 April – 30 April

Source: Data from Refinitiv, annotation by Equilibrium

Of course, this is an unfortunate situation of timing rather than any attempt to fix the numbers. Indeed, there are an equal number of times when the opposite happens which would appear to reduce our relative performance.

Mitigation

Asset markets have moved to quicker pricing and settlements of transactions over the years, but progress is slow and, unfortunately, we are unlikely to be in a situation when all assets are priced at 12 noon at once in the near future.

However, these timing gaps tend to iron themselves out over time and only become amplified over short-term time periods, especially around times of high volatility (large movements up and down) in markets such as we have seen recently.

Thus, looking at our performances over longer and different time frames will significantly reduce these timing effects and give a more accurate basis for comparison.

Past performance is never a guide to future performance. Investments will fall as well as rise. Any performance targets shown are what we believe are realistic long-term returns. They are never guaranteed. The information contained in this publication is based on the opinions of Equilibrium companies and does not constitute advice. Please contact your adviser before taking any actions.