Colin Lawson

Colin Lawson

In the wake of recent events and their implications for portfolios, many clients are asking, if we are over the worst, how quickly recovery will happen and in what shape it will take. I want to share some reasons for optimism tempered with some caution about what this could look like.

In July last year, we produced the slide below for our quarterly market update which indicated that if this was a typical bear market (there is no such thing by the way) that it would end on the 19th October 2022.

It was not meant in any way to be a prediction. If, however, we believe that the bear market has ended, then it may have done so a week early, as the low point (let’s hope it’s the low), occurred on the 12th October 2022. The recovery that has happened in our portfolios since then can be seen in the table below.

| Fund | Growth % (12/10/22 - 13/02/23) |

|---|---|

| Equilibrium AIM Portfolio | 20.31 |

| Equilibrium Adventurous Portfolio | 10.24 |

| Equilibrium Global Equity Portfolio | 10.21 |

| IFSL Equilibrium Balanced Portfolio | 9.58 |

| IFSL Equilibrium Cautious Portfolio A Acc in GB | 8.30 |

| Equilibrium Positive Impact Portfolio | 7.43 |

| IFSL Equilibrium Defensive Portfolio Class A Acc | 5.19 |

Source: FE Analytics

Last year, at our November quarterly market update we also shared this slide that shows what has happened historically in the following 24 and 36 months after portfolios suffered significant losses over a 9-month period. There are 133 9-month periods, so we have a fairly significant data set to work with.

The shape of the recovery is similar for our other funds with the greatest gains following the greatest losses.

Whilst this brings me a degree of confidence that the recovery is happening and is likely to replace the losses in fairly short order, we must be cautious. The road to recovery is usually littered with setbacks, diversions and even the odd roadblock.

When we look at the preceding two bear markets, the Credit Crunch and Covid-19, the catalyst for markets to bounce back was huge stimulus from the central banks in the form of quantitative easing.

With Covid, we had the added advantage of a vaccine.

This time we don’t have those magic bullets.

This time, we’ll have to grind our way out the hard way and the variety of data points being watched means it’s more likely to be a bumpy ride. These include but are not limited to:

1. Inflation starting to fall and heading towards zero or negative numbers.

All the data we have leads us to believe that this is already happening.

2. Pay rises being constrained

So far, the government and companies are holding firm, but the shortage of jobs (caused by Brexit/ Covid retirees/ demographics) in certain sectors is leading to pockets of significant increases which remains a concern.

3. Interest rates and Gilt rates

So far, the signs indicate that central banks are approaching the peak of the cycle, which will leave them room to cut interest rates in the future. It’s a careful balancing act that involves slowing the economy and then cutting rates quickly enough if they go too far. The Gilt rate, which is the cost the government borrows at, is arguably more crucial as it can have a bigger effect on the mortgage market as well as pension funds and annuities.

4. Government borrowing

As we saw from the disastrous mini-budget, if the market loses confidence in the government’s ability to navigate through these tricky times the implications can be severe.

5. The economy

So far, the indications suggest that any recession will be shorter and shallower than first feared or could even be avoided all together.

6. Corporate earnings

How well will companies’ profits hold up against expectations?

7. Corporate failures

In the absence of significant government and central bank support, a number of companies may go bust. In the long run, this may not be a bad thing, but in the short term, it can affect sentiment.

These points are the seven key things to watch in any economy, and if we focus on the G7 economy alone, that’s potentially 49 regular pieces of significant information for traders and markets to digest.

Summary

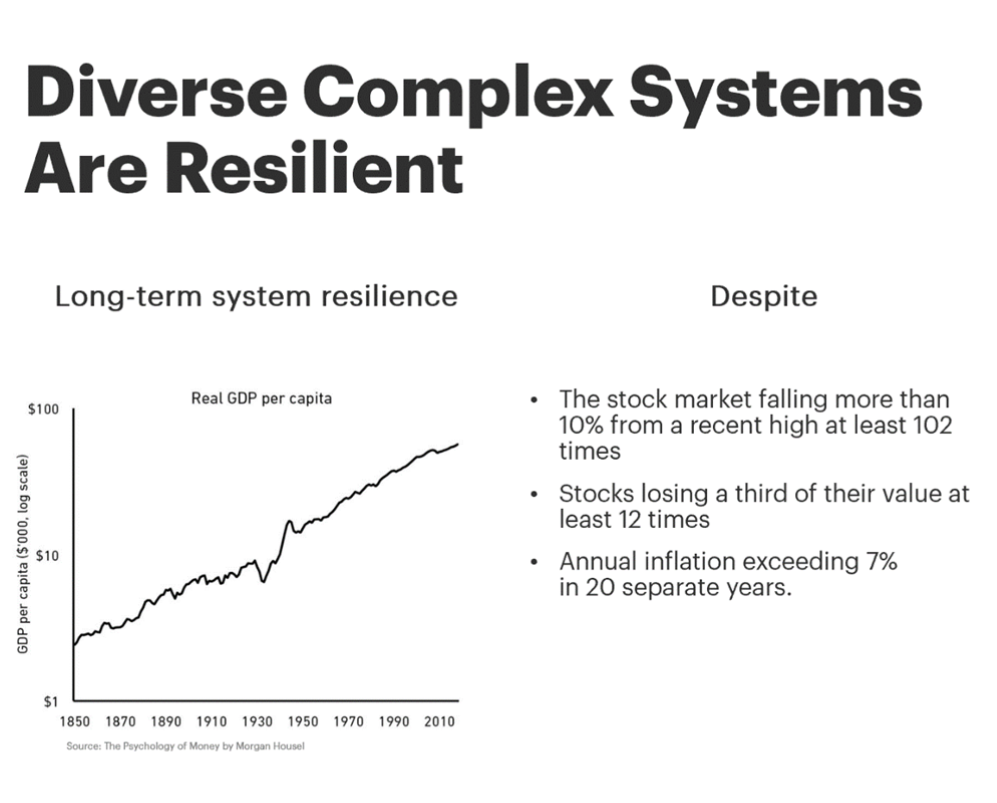

One thing you can count on is the recovery not being in a straight line, with many sensationalist headlines and some scary bumps along the way.

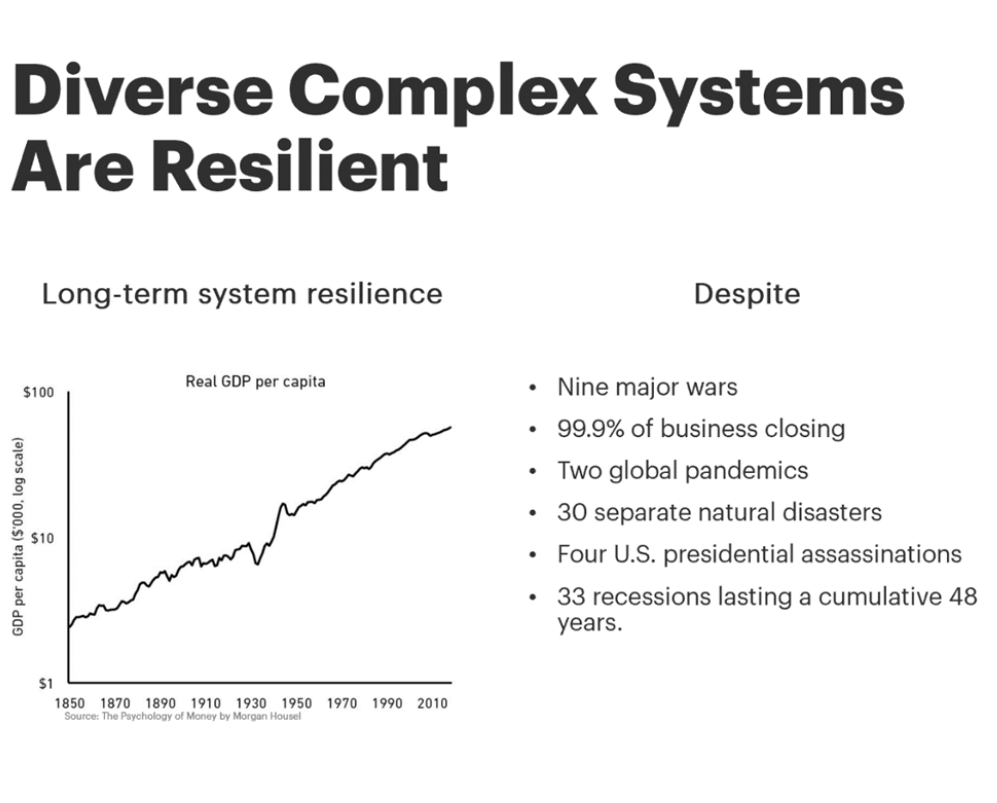

But you can also count on the recovery itself. We have faced many bigger challenges in the past and gone on to thrive as you can see from the charts below.

We will do everything we can to keep you up to date and to guide you and your portfolios over the months and years ahead.

This blog is intended as an informative piece and does not constitute advice. If you have any further questions, please don’t hesitate to contact us. If you’re a client you can reach us on 0161 486 2250 or by getting in touch with your usual Equilibrium contact. For all new enquiries please call 0161 383 3335.