Mike Deverell

Mike Deverell

Executive summary

- Enhancing return usually involves accepting increased risk and conversely, lower risk tolerance means accepting a potential lower return.

- Volatility is just one type of risk, often seen in liquid assets like shares. Illiquid assets are less volatile but can carry a greater risk such as catastrophic loss.

- We think the best definition of risk is “uncertainty” and we try to minimise uncertainty in portfolios, despite the inherent unknowns.

- We increase predictability through assets such as defined returns which provide a pre-defined return provided certain conditions are met.

- For example, we recently purchased a UBS product offering 11.65% p.a. return if the FTSE 100 and S&P 500 are at or above 8,271 and 5,472 respectively at any one of 10 specified dates over the next five years.

- This product offers greater certainty and potentially higher returns compared to equities, based on the history of these markets since the 1970s.

- The biggest risk in this case is that the market indices could outperform the 11.65% return of the product.

- Conversely, markets could do worse than expected, which would affect defined returns in the short term, however, the risk of loss over the long term is minimised by the capital protection in the product.

- Another risk to be aware of is counterparty risk should UBS go bust which, whilst a remote possibility, would be catastrophic and for this reason we would never put more than 5% of our money in any one investment bank.

- However, in an uncertain world and amidst ever-changing geopolitical events, we think sensible use of these products helps to balance the unpredictable nature of investments for those able to take a long-term view.

The power of predictability

We are always looking for ways we can enhance returns for clients.

In particular, we focus on risk-adjusted returns. In general, to increase the potential return of a portfolio we have to also accept increased risk. Or to put it another way, if we can’t stomach a certain amount of risk, we might need to accept a lower return!

The term risk is often used interchangeably with “volatility”, which is how much an investment goes up or down in the short term.

But volatility is only one type of risk. Generally, very “liquid” assets like company shares can be volatile, simply because they are traded so frequently. Each trader will have a different view on what the shares are worth, hence why the price goes up and down so much.

Less liquid assets tend to be less volatile, but instead there is the risk that you might not be able to get your money back when you need it. There is also often a greater risk of “catastrophic loss” in illiquid assets, where everything seems fine right up until the point when it isn’t! Illiquidity means you just have to sit there and watch if things go wrong and are unable to react.

To us, the best definition of risk is “uncertainty”.

When running the portfolios we try to reduce uncertainty as much as we can. Clearly, without a fully functioning crystal ball there will always be plenty of unknowns, but there are also ways we can reduce the range of potential outcomes.

Predictability in an uncertain world

One way we can increase predictability is to use assets like defined returns.

For those that aren’t familiar, these are a type of “structured product” which provide a pre-defined return in a given set of outcomes.

For example, we recently purchased a defined returns product from UBS, the Swiss investment bank. This was created especially for clients of Equilibrium after we approached our panel of different banks and let them compete against each other for our business.

This UBS product was set up on 9 September, when the FTSE 100 was at 8,271 and the S&P 500 was at 5,472.

The product will pay us a pre-defined return of 11.65% p.a. (not compound) should these two markets be at or above these levels at any one of 10 specified dates over the next five years. The markets don’t have to go up, just sideways, in order to get our money back plus the defined return.

The first potential kickout date is 10 March 2025. If the markets are the same or higher at this point, we’ll get our money back plus a gain of 5.825% (half of 11.65%). If not, the product rolls on to the next date (9 September 2025) when the potential return will go up to 11.65%.

The potential kickout dates are every six months over the next five years, with the return increasing by 5.825% every time it doesn’t kick out.

If we get to the end of five years and the markets have never been higher than the start point, we’ll simply get our money back unless one of the markets is down more than 40% over the term. In that case, we’ll get the market return, for example, if one of the indices is down 45%, we’ll lose 45%.

This is an attractive investment in our view. At current market levels, our best guess is that stock market returns over the next couple of years might be in the mid to high single digits, somewhat less than the 11.65% p.a. potential return of this product.

There is also much greater certainty around this product than by investing directly in the stock market. Not only do we know what return we’ll get in a certain set of circumstances, but the chance of getting a double-digit return appears to be high.

We can say that with a reasonable degree of confidence, as we can back test the structure and see what might have happened in the past.

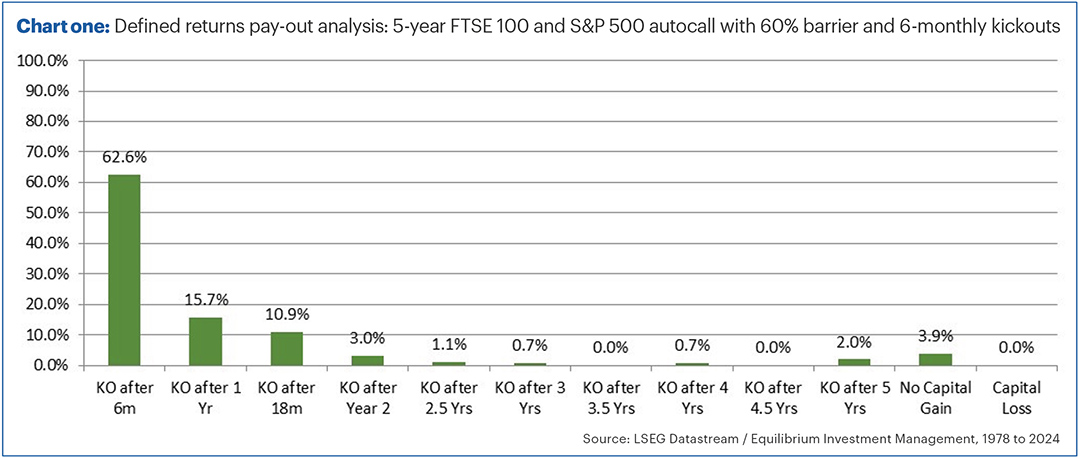

Chart one shows how frequently we’d have got our return at different stages, looking at the history of these markets since the 1970s.

Most of the time in the past we would have had kick out (when the product matures) in the first two years (over 92% of the time).

Crucially, only 3.9% of the time historically would we have got to the end of five years and not achieved a positive return. These instances were mainly those beginning in around 2000, after the tech bubble burst. We have never had a product not give us a return since we began investing in them in 2011. The products can also be traded daily and so we could potentially sell early if required.

At no point would we have been down 40% over five years, meaning we’d never have lost money on the product.

So, what are the risks?

The above is based on historic data. The future might be very different to the past, even though our analysis is based on a large data set with a long history.

However, in our view, the biggest risk is a relative one. For example, the FTSE 100 or S&P 500 index on which this product is based could go up a lot MORE than 11.65%. If the markets go up (say) 20% over the next year, we still only get 11.65%.

We’re feeling a bit cautious about stock markets after a decent run, with some parts of the market looking quite expensive in our view. We therefore wouldn’t be surprised if there was a bit of a pull back at some point, although taking a two-year view, we still think equity markets will most likely be higher than now.

Based on this, we prefer the defined returns to a direct equity investment. However, that’s just our opinion, even if it’s based on data and analysis.

We might also be wrong in the other direction, and markets could do a lot worse than expected. In the short term, that wouldn’t be good for defined returns as these are daily traded instruments, meaning they will go down in price if the market falls. However, that’s merely “volatility”. The risk of loss over the long term is reduced by the capital protection inherent in the product.

There is also counterparty risk. In the above example, we have taken out a contract with UBS. If UBS were to go bust, they might not able to pay the contracted returns or give us back our capital. There is therefore a risk of “catastrophic loss”.

However, we think the chance of UBS defaulting is pretty remote. We think regulators will step in if there is even a whiff of trouble, as happened when Credit Suisse failed a couple of years ago. Note, all of Credit Suisse’s structured product terms were still fulfilled.

Nevertheless, this risk is real. As a result, we never put more than 5% of our money with any one investment bank. We also monitor the default risk of the banks and only use ones we deem to be highly secure.

We usually will have some of the portfolios in defined returns, but at present we have more than usual. It is close to 15% of the balanced portfolio, and around 20% of our global equity fund at present. This is due to our view of the relative attractiveness compared to traditional equities.

The world remains very uncertain, especially with the US presidential election coming up, as well the UK Autumn Budget, along with various central bank meetings, all of which could affect our investments (for good or ill!).

However, sensible use of products such as these reduce some of the unpredictability that is inherent in investments, for those able to take a long-term view.

Past performance is for illustrative purposes only and cannot be guaranteed to apply in the future.

This newsletter is intended as an information piece and does not constitute a solicitation of investment advice.

If you have any further questions, please don’t hesitate to contact us. If you’re a client, you can reach us on 0161 486 2250 or by getting in touch with your usual Equilibrium contact.