Mike Deverell

Mike Deverell

Executive summary:

- Predictions for the UK economy are generally lower than those for other developed nations.

- We also appear to have been more vulnerable to rising inflation than many other countries.

- Various reasons have been cited, such as Brexit, recent political turmoil, and falling labour participation after the pandemic.

- However, the main drivers of high inflation – food and energy – are likely to see falling prices soon.

- Because of the negative view on the UK economy, many international investors have been avoiding the UK.

- However, this means that many UK assets look cheaper than equivalent firms elsewhere.

- International Private Equity firms now seem to be seeing the value – with many recent bids for companies and property firms.

- Might this bode well for UK market returns, as bargain hunters look to buy cheaply?

Can Britain be Great again?

The recent coronation of King Charles III was a moment of celebration for many people. At the very least, I’m sure most of us appreciated the extra bank holiday!

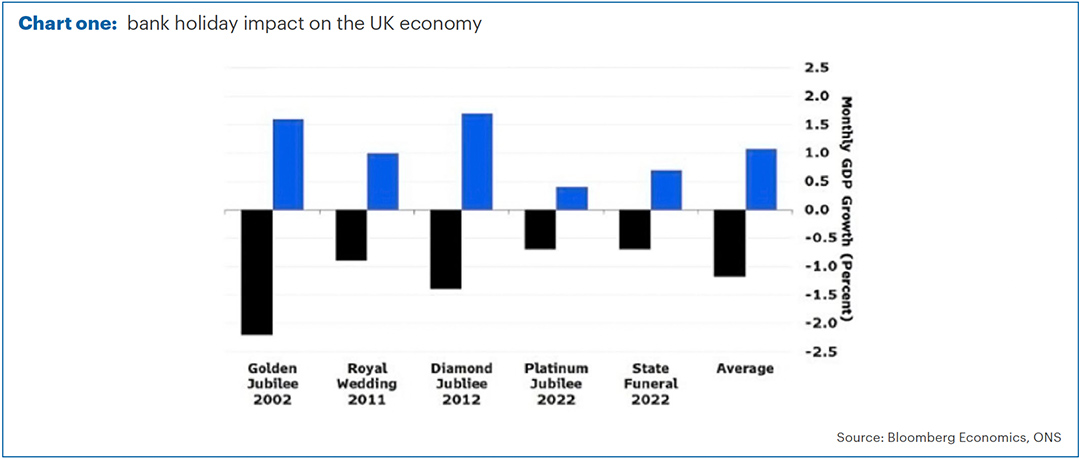

However, the extra day off is likely to have a less than positive impact on the economy. Chart one shows that when we’ve had additional bank holidays previously, the economy has tended to shrink. However, it does tend to bounce back somewhat the following month.

Whether or not they took this into account, when the International Monetary Fund (IMF) released their latest economic forecasts, it did not paint a rosy picture for the UK.

Whilst they predict that the global economy will expand by 2.8% in 2023, they think the UK economy will shrink by 0.3%. For 2024, they expect 3% economic growth globally, but only 1% for the UK. (Source: IMF)

Part of this is due to high inflation, which appears to have hit the UK harder than most.

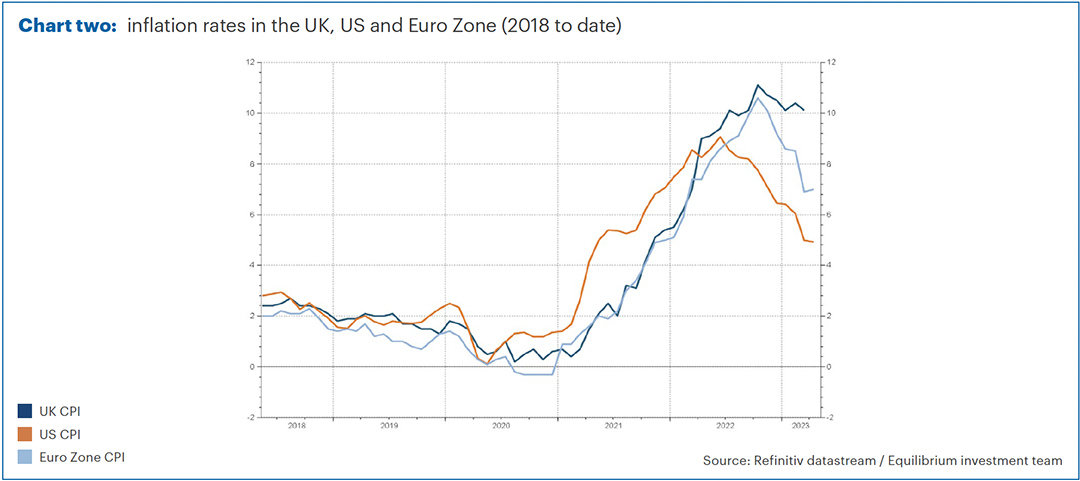

Chart two shows Consumer Prices Index (CPI) inflation in the UK in dark blue, compared to the US in orange and Euro Zone in light blue.

UK inflation peaked at 11.1% in October 2022, whilst Euro Zone inflation peaked at 10.6% in the same month. US inflation peaked earlier, at 9.06% in June 2022.

Not only was our peak inflation higher, but we can also see from the chart that European and US inflation has since been falling sharply, whilst ours remains above 10% (as of the end of March 2023).

Food and energy

We’ve discussed previously in The Pulse how energy prices have been the biggest contributor to UK inflation. This was also an issue in the rest of Europe, but less so in the US.

Various European governments have dealt with rising energy prices in different ways. Here in the UK, the price-cap mechanism on energy bills has the effect of smoothing out price rises but also means a delay in passing on the recent fall in wholesale energy prices.

As well as energy, rising food prices are also having a big impact. In March’s inflation figures, food and non-alcoholic beverages accounted for 2.3% of the 10.1% headline inflation. (Source: Office of National Statistics)

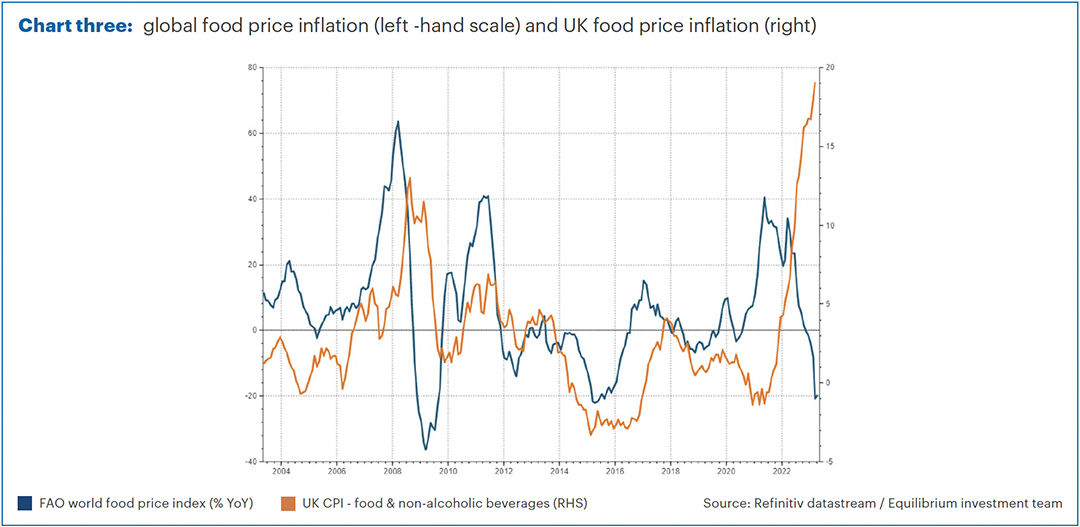

Chart three shows the year-on-year inflation in world food prices – according to the UN’s Food and Agriculture Organization (FAO) – in blue, compared to the food and non-alcoholic beverages component of UK inflation in orange (right-hand scale).

Global food price inflation peaked in late 2021 and, whilst it remained high for much of 2022, it has now turned into deflation. Meanwhile, UK food prices are 19% higher than a year ago.

The good news is that the two lines do tend to follow each other but with a lag of perhaps 12 to 18 months. Falling world food prices should hopefully be reflected in UK shops soon, and indeed we are seeing signs of some recent price cuts.

With the energy price cap also likely to fall when next reviewed in July, we think inflation could drop quite rapidly later this year.

What is wrong with the UK?

The big question is whether there is something about the UK which has made us more vulnerable to economic shocks such as this?

We are, of course, an island nation. Naturally, we will therefore need to import certain commodities or goods and so can be vulnerable to supply chain issues.

The pound also fell sharply last year – increasing import costs – although it has recently rebounded somewhat. Sterling has generally been weak since the Brexit referendum in 2016 and has suffered periods of volatility since. Brexit itself may also have increased import costs through increased red tape.

Some of these factors may have contributed to the “salad shortage” we saw earlier this year. At the time, this was variously blamed on bad weather in the Mediterranean, exporters favouring European markets over the UK and higher energy prices making indoor growing less economical. In truth, it was probably a combination of all of these.

One area where the UK certainly seems to stand out compared to our peers is the labour market.

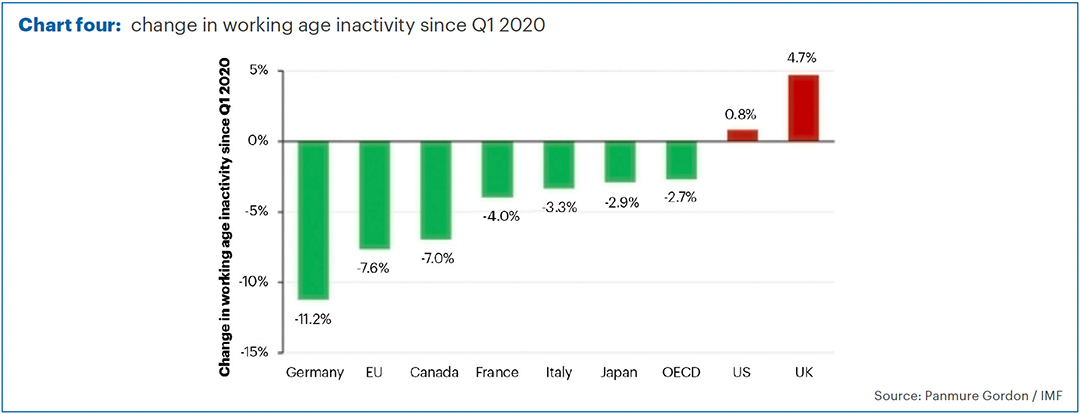

Since the pandemic, there has been a sharp increase in the number of “inactive” people of working age in the UK, with more than half a million people dropping out of the labour market since 2020. Chart four shows how this compares to other countries, most of which have seen inactivity fall when ours has risen. (Source: Panmure Gordon)

This “inactivity” appears to be through a combination of ill health and people choosing to retire early, although the exact cause is hotly debated.

We have also seen a trend of foreign workers leaving the UK during the pandemic and not returning.

In theory, all this could be inflationary as a smaller workforce should mean increased bargaining power for employees. However, whilst we are seeing rising wages, average increases remain well below inflation. To see a 1970s-style wage-price spiral would normally require wage hikes above price inflation.

However, these factors may well be contributing to the sluggish growth outlook and perceived poor productivity.

UK assets

Whatever the reasons, international bodies such as the International Monetary Fund (IMF), as well as international investors, seem to have a gloomy view of the outlook for the UK.

This is also reflected in the value of UK assets, and not just through the weaker pound.

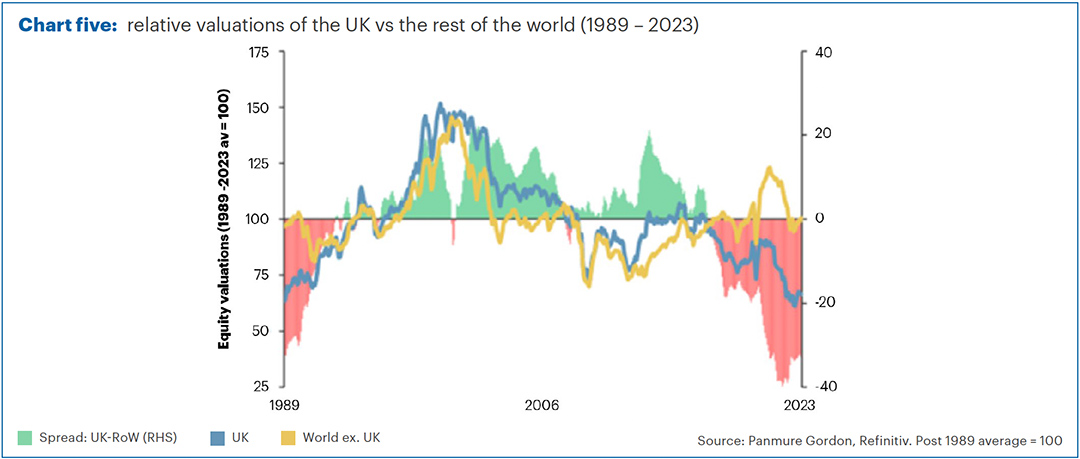

Chart five shows the relative valuation of the UK stock market vs the rest of the world, and how this has changed since 1989.

For much of the 1990s and 2000s, the UK stock market traded at a premium compared to the rest of the world (where the shaded area is green). Over the past few years, this has moved to a discount (the shaded area is red) and now the UK market is valued much more cheaply than other markets.

As you can see, after the Autumn Mini-Budget, the “UK discount” was as much as 40%, although it has closed a bit since.

According to stockbroker Panmure Gordon, only part of this can be explained by the makeup of the UK market. For example, we have very little in fast-growing technology sectors, which tend to command a premium.

However, the discount seems to persist across every individual sector. For example, a UK energy firm would be valued less than an international energy firm, a UK bank cheaper than an overseas bank, etc.

Whether this is due to recent political instability, Brexit, demographics or something else, we can see the recent effects of this.

ARM is one of the leading designers of microchips in the world, based in the UK (in Cambridge). It was previously listed in London but was bought by the Japanese conglomerate Softbank in 2016.

Softbank is now looking to sell part of its ARM holding by listing it again. Despite lobbying from the London Stock Exchange and the UK government, Softbank has decided to list ARM on the US stock market. The reason is that they will probably be able to sell for a higher valuation.

Listing on the US rather than the UK market doesn’t change the underlying business in any way but does make it more attractive to certain investors. This may seem irrational, but not if you’re Softbank looking to achieve the best price!

Bargain basement

The question is whether some UK companies are being “unfairly” overlooked, simply because they are listed in the UK? If so, does this represent an opportunity for patient investors?

There are certainly signs that some international investors are starting to see value.

In particular, we’ve recently seen two real estate investment trusts (REIT) approached by private equity buyers from overseas. A couple of months ago, Industrials REIT agreed a deal with Blackstone, the large American investor, at a 42% premium to the share price on the date of the bid (31 March 2023).

More recently, the Civitas Social Housing Investment Trust received an offer from CK Asset Holdings, whose chairperson is Li Ka-Shing, named by Wikipedia as the 38th richest person in the world. The share price jumped 48% on the day.

We didn’t hold Industrials REIT (although we hold others in the same sector), but we did hold Civitas. Rather than wait for completion, we exited our holdings on the day the bid was announced with nearly the full takeover value (79.7p compared to the bid of 80p per share).

These are both property trusts where the share price was trading at a significant discount to net asset value – the market value was well below the value of the underlying buildings.

Whilst this makes the value in these assets quite visible, we are seeing similar bargain hunting in non-property businesses.

Recently, THG (formerly The Hut Group) received a bid from private equity company Apollo, pushing the share price up 40% in a day. Private equity has also bid for several other stocks recently, such as credit card processor Network International, Dechra Pharmaceuticals and energy services business Wood Group. Interestingly, the management teams of THG and Wood Group have rejected the bids stating they don’t reflect the full value of the businesses. (Source: FT)

In the long term, seeing UK-listed businesses taken private might not bode well for market liquidity. However, it shows that overseas buyers are seeing the value here in the UK, which, in our view, could be a catalyst for better returns ahead.

Past performance is for illustrative purposes only and cannot be guaranteed to apply in the future.

This blog is intended as an information piece and does not constitute a solicitation of investment advice.

If you have any further questions, please don’t hesitate to contact us. If you’re a client you can reach us on 0161 486 2250 or by getting in touch with your usual Equilibrium contact. For all new enquiries please call 0161 383 3335.