Mike Deverell

Mike Deverell

This article is taken from our spring 2020 edition of Equinox. You can view the full version here.

For the past few years, we seem to have been using the word “uncertainty” a great deal!

Currently, we are all worried about the impact of the COVID-19 coronavirus, both on a human and an economic level.

However, even before we heard about this virus, political and economic uncertainty was elevated. For the last few years investors have been concerned about the impact of Brexit and the so-called trade war between the US and China.

What all these things have in common is that they are highly unpredictable, with a wide range of possible outcomes in terms of seriousness and impact.

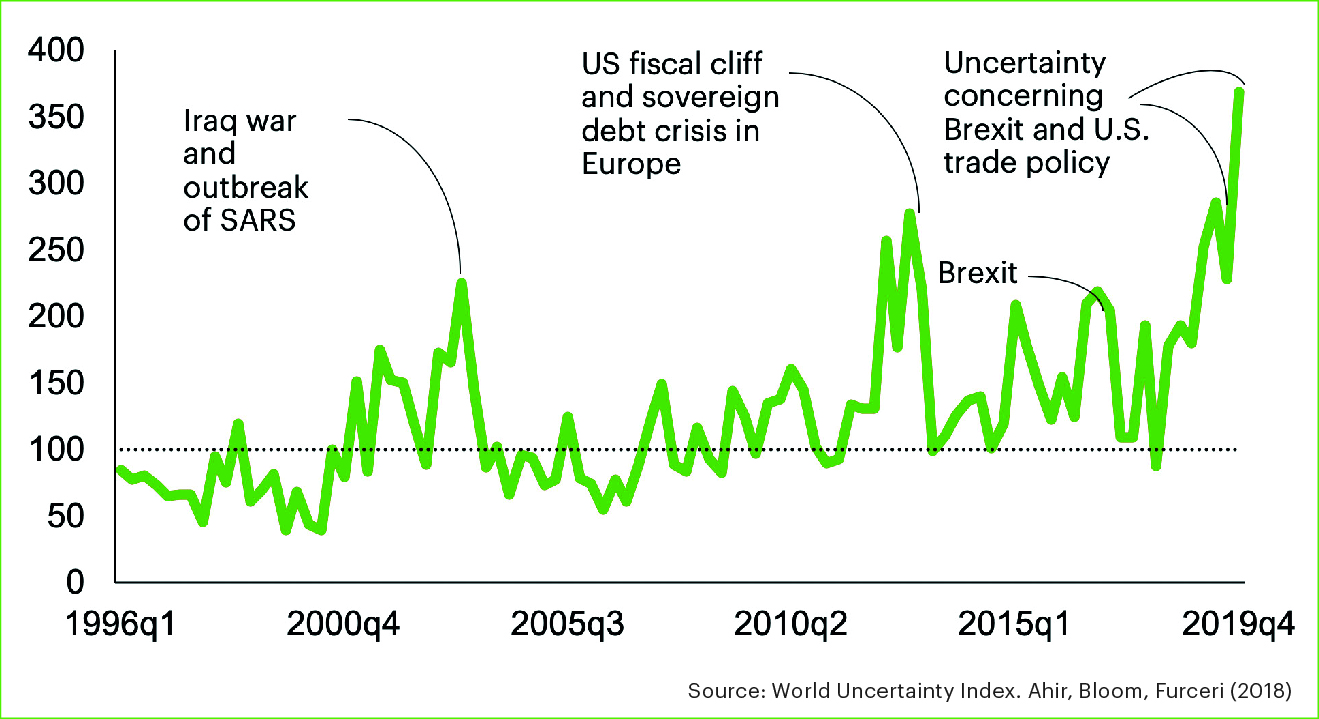

The International Monetary Fund runs a ‘World Uncertainty Index’ which measures economic and political uncertainty. Every year the IMF produces reports outlining the outlook for various countries across the globe. It simply looks at how frequently words like ‘uncertainty’ are used in these reports.

The data goes back to 1996. According to this index (chart one), uncertainty as of the end of 2019 was higher than it had been at any other time in that period.

After the trade agreement between the US and China and the UK general election, we thought this uncertainty might come down in 2020. So far we have been proven incorrect on this one!

Supposedly, the Chinese word for “crisis” is made up of two characters. One is the symbol for “danger” the other for “opportunity.”

This may be a Western misinterpretation, but even if incorrect it sums up the way we feel about uncertainty.

We firmly believe that those investors who can afford to take a long-term time horizon or have a high tolerance for risk now have a great opportunity.

There is the potential to buy into those admittedly higher risk but higher potential return investments, at a much cheaper price than we have seen for several years.

In most walks of life, when things are on sale for 20% cheaper than before, we think it’s a bargain. In the stock market, as humans we find it much harder to buy after a market fall, even though the same principle still applies. At Equilibrium, we believe that a crisis means there are some potential bargains to be found.

Your future financial confidence

We see giving clients clarity and confidence around their finances as one of our key roles.

In the face of the unsettling environment the ‘confidence’ element of our job has been made much more difficult! Over the past couple of years, some clients have wanted to reduce risk in their investment portfolios in order to reduce some of the uncertainty.

Given the way things have panned out so far in 2020, those clients who did so are most likely to be better off. Higher risk investments have naturally been hit hardest by the recent market turbulence.

Whilst the virus is highly concerning, the economic effects are likely to be in the shorter rather than long term. On the other hand, we now have a bit less uncertainty around Brexit and global trade, and have governments and central banks that are providing massive levels of stimulus.

Over the very long term, equity and related investments have tended to outperform lower risk investments by a significant margin. Investors who can afford to take that long- term view may therefore see market sell-offs as a buying opportunity.

Risk assessment

Deciding how much risk to take is an art, not a science. We need to take into account your emotional tolerance (how losses make you feel), your capacity for loss (can you still pay the bills if the portfolio goes down?), the return you need to achieve your goals over the long term and your desire for risk.

However, one of the key variables is the time horizon.

If you need a chunk of money out of your portfolio in the next year or two, then it makes sense to keep an appropriate amount in cash. We simply don’t know what will happen in markets over the next couple of years and we don’t want people to be forced to sell at the bottom if they need the access to funds.

However, if you are in your forties and not planning to retire until your sixties, then you may have twenty years until you need to touch your pension portfolio. In such circumstances, many investors can probably take more risk than would be indicated by a simple risk tolerance questionnaire!

Our global equity strategy

We believe now is a good time to be launching our new investment strategy.

This strategy is designed to produce long-term growth and aims for returns in line with (and hopefully in excess of) global equity markets, but with less volatility. Our global equity strategy is made up of funds that are contained within our other portfolios but is a more concentrated mix.

The strategy is roughly 80% in equities, with a further 10% each in defined returns and alternative equity. We can then use the alternative equity funds to ‘volatility trade’ in and out of equities, buying on dips and selling on recoveries. At times of market lows the portfolio could be 100% in equities if we felt that was the correct approach.

Because of the way it is constructed, we can produce some meaningful backtesting based on actual investment decisions we made in our other portfolios.

Based on this backtesting, we believe that the portfolio can produce equity-like returns but with roughly 80% of the volatility of a typical global equity fund.

Time in the market or timing the market?

We believe that now is as good a time as any to launch this strategy.

Whilst we are in the middle of a turbulent period, markets tend to over-react and this creates value for selective investors.

In particular, we think there are fundamental reasons why emerging markets and the UK should outperform, given some of the concerns about such regions have eased.

Whilst stock markets have got cheaper so far in 2020, bond markets have become more expensive. At the time of writing, a 10-year UK gilt yields just 0.3% pa. This is the return you would get if you bought a UK government bond and held it for an entire decade. It would almost certainly lose you money in real terms.

As a result, those building up a pot for the future certainly can’t rely on bonds. The only way to increase the returns is to increase risk, and often that means holding more equities. However, we believe we can still diversify a portfolio by also using alternatives such as infrastructure and absolute return strategies.

We can also make extensive use of defined returns.

Defined returns

Defined returns are structured investments which can provide a fixed level of return depending on what happens with stock markets.

For example, we have recently struck a new product with Goldman Sachs in many of our portfolios.

The product was set up on 11 March 2020 when the FTSE 100 was at 6,000 and the S&P 500 was at 2,808. If both markets are at or above this level on 11 March 2021, the product will end on that day and provide a 20% return.

markets tend to over-react

This means the markets can go sideways for a year and we still get a very high return. Of course, that rate is particularly high because we struck the product when the markets were extremely volatile, but we aim to buy products with headline returns in excess of at least 10% per annum even in less volatile times.

If the market is below 6,000 (FTSE 100) and/or 2,808 (S&P 500) on the first anniversary, the product rolls on to 11 March 2022. Should both markets be above their start point on that date the possible return is now 40%.

There are six chances for this kickout to happen. If the market only just scrapes back above 6,000 / 2,808 in six years’ time, we have a potential return of 120%!

If we are still below those levels after six years the investment provides an assurance of return of capital, unless one of the markets is down 40% or more on that date. Credit risk is also a factor. By purchasing defined returns products we are entering into a contract with an investment bank and as such the products also have counterparty risk. Please speak to your usual Equilibrium contact for more details of the risks

By purchasing defined returns products, we are entering a contact with an investment bank and, as such, the products also have counterparty risk. Please speak to your usual Equilibrium contact for more details of the risks.

In our view, by using defined returns and other alternatives, our new strategy should be able to produce equity-like returns but with less risk overall.

Launch date

We are aiming to launch this new strategy as a fund with a current target date of mid-May. The IFSL Global Equity Portfolio Fund will sit alongside our existing range of three fund portfolios. Investment Fund Services Limited (IFSL) are part of the Marlborough Group and, as with our existing funds, will provide ACD (authorised corporate director) services to run the fund on our behalf.

However, the opportunity to buy at such low prices may be short lived. We have therefore decided to launch a model portfolio with immediate effect, so that our clients can switch in to the strategy at relative lows.

This will involve a little more work for us in the short term, but we believe it is the right thing to do for our clients.

For existing clients, if we believe you are suitable for our new strategy, we will be in touch at the appropriate time. We may then recommend you switch out of the model portfolio and into the new fund once it is launched.

In the meantime, if you have any queries please get in touch with your usual Equilibrium contact.

Chart one: IMF World Uncertainty index