Mike Deverell

Mike Deverell

Human beings love a great narrative.

Investors are often drawn to stories about the “next big thing” that will change the world.

Sometimes, those “next big things” do turn out to be revolutionary but that doesn’t always make investing in them easy.

In July 1995, as internet use moved into the mainstream, a little online bookshop, now known as Amazon, was launched. Initially operating from the garage of a house in Seattle, by October that same year, Amazon.com had sold books to all 50 states of the US and to 45 other countries.

In May 1997, the company floated on the Nasdaq index. Had you invested £100 at that point, your investment would currently be worth a cool £157,909. (1)

A great story and a great investment, right? Whilst Amazon was at least founded on sound business principles – they actually sold stuff (!) – in the late 1990s, many other web-based companies were launching without much of a plan for making any money. And investors were bidding up anything with dotcom in its name.

As the Wall Street Journal reported in May 1999:

“One of the sacred tenets of business – you have to make money – suddenly looks almost like a quaint artefact of an outdated era.”

From 1 January 1998 to 27 March 2000, the tech-heavy Nasdaq 100 index went up by 253.73%. (2)

Then, the bubble burst. It’s difficult to say why. Perhaps investors just came to their senses. Regardless, from 27 March 2000 to 7 October 2002, the Nasdaq fell by a total of 82.9%. (2)

Had you invested in the Nasdaq in March 2000, it would have taken you until 2015 to get back into the black.

And Amazon? From 1 January 2000 to 28 September 2001, it dropped a massive 92% and it took until 2007 to make back those losses.

And what about the other market leaders from back then? Where are AOL and Yahoo these days?

Investing in stories is hard. Investing in the right companies, at the right time, is even harder.

Evidence-based investors

Investors who looked at the data back then would have most likely reacted differently to those who followed the narrative.

As of January 2000, the S&P 500 (the main US stock market) traded at a price/earnings (P/E) ratio of 30. This means that the total value of the 500 companies was 30 times the annual profits they made at the time.

The average P/E ratio between January 1973 and December 1999 had been 14 times earnings, so the market was more than twice as expensive as usual. A wise investor might have looked at this and decided that, whether or not the internet might change the world, 30 times was just too much to pay for the chance to participate.

After the bubble burst, valuations went back to more normal levels.

The P/E of the US market didn’t get back above 30 times again until late 2020, peaking at 35 times earnings in mid-2021. (3)

During 2022, the S&P 500 fell by over 24% from peak to trough, from 1 January to 12 October 2022.

The valuation of the market tells you a lot about future returns, but often you need a long-term perspective. In the short term, markets often overshoot what is rational by a huge margin, both when they go up and when they go down.

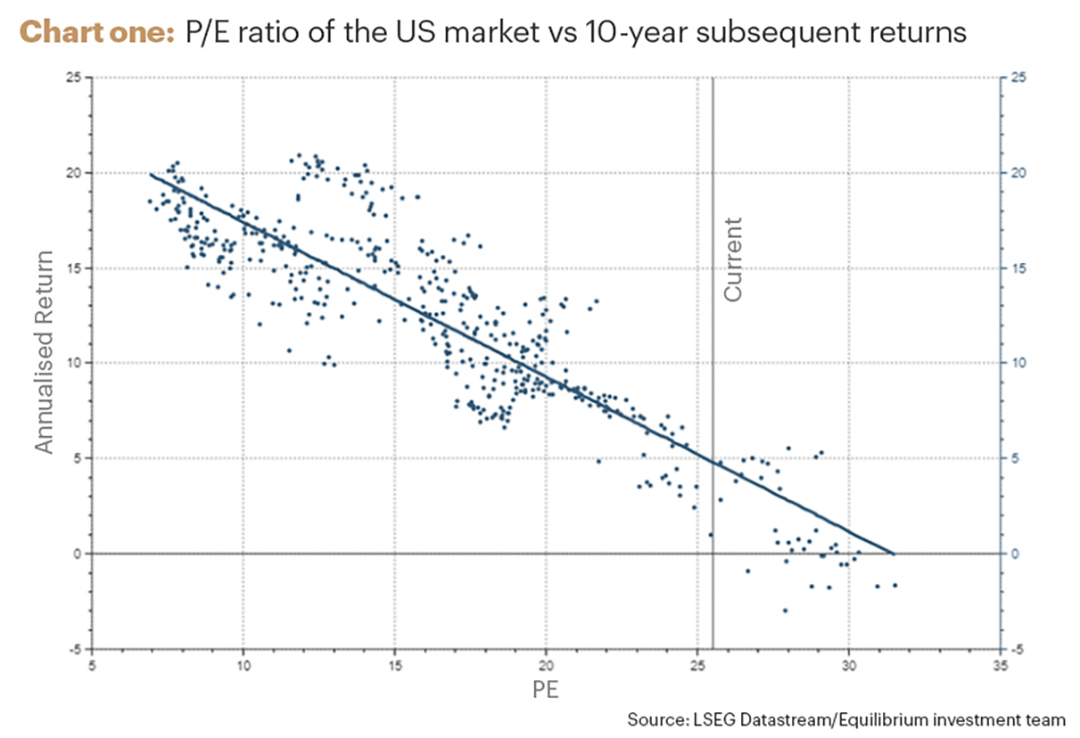

Chart one shows the relationship between the P/E ratio of the US market, relative to 10-year subsequent returns. Each dot is a different 10-year period in history, and the higher the dot, the higher the return over that period.

Along the horizontal axis is the P/E ratio of the market at the start of that 10-year period. Cheaper valuations are to the left, and more expensive ones are to the right.

The dots tend to be a lot higher when you start with a cheap market, and a lot lower when you start with an expensive market.

Start at 30 times earnings, and you’ve never made money over 10 years. Investing is easy, right?

Rise of the robots

In 2023, the narrative for investors was all about artificial intelligence (AI).

Like the internet which came before it, as AI became mainstream through the launch of services like ChatGPT, investors became excited about the prospects for those companies thought most likely to profit.

But unlike the tech bubble, this time investors think that some of the largest companies in the world are those most likely to benefit. The so-called “magnificent seven” big tech stocks in the US went up a cool 96% in 2023. (4)

By the end of the year, these seven companies represented nearly 30% of the S&P 500, (5) helping to drive the market up 18.58% during the year. (6)

Reading this, you may ask: “If nearly a third of the market pretty much doubled, shouldn’t the market be up 30%+ rather than 18%?”

What this tells you is that the other 493 stocks in the index haven’t done nearly as well.

For example, an equal-weight version of the S&P 500 – where you invest the same amount in each of the 500 companies – was only up 6.7% over the same time period.

2023 was a good year for US equity investors, but the leadership was extremely narrow.

The price/earnings ratio of the top seven is now 48 times reported earnings. (7) The market as a whole is on 24 times, still pretty expensive, but skewed by the big seven.

AI may change the world. It may make us all much more productive, and allow certain tasks to be completed more quickly, without human intervention. But we have yet to see much evidence of increased revenues for most of these companies as a result.

We do not know what will happen next, but the evidence from history says we should be cautious.

Golden rules of investing

We have a list of our “golden rules of investing.” The investment team will frequently refer back to this list and we find doing so really helps our investment decision-making. In particular, it helps us avoid what look like attractive investments on the face of it, but where something doesn’t quite stack up.

Here are just a few of our golden rules, some of which you’ll already have worked out from this article:

- Decisions must be evidence-based. Most asset classes have some valuation indicators that give you a broad idea of the future. Our advice is to use them.

- Look forward not back – allocate based on the likely future return, not past returns.

- Diversify your portfolio widely because you will often be wrong.

- Outperformance comes from being right more than you’re wrong and, more importantly, making more money when you’re right than you lose when you’re wrong.

- Utilise known advantages. There’s a vast amount of academic research out there showing what drives markets. For example, this shows that small companies will outperform large companies over the long term and that exposing your portfolio to greater growth drives long-term portfolio growth (e.g. emerging markets).

- Past performance is no guide to the future – but past behaviour is often a guide to future behaviour.

In summary, we like to construct diverse portfolios, exposed to lots of different asset classes, sectors and currencies, with a bit more than most in smaller and emerging companies.

Our portfolios did fairly well last year, but perhaps we could have done better had we ignored these rules! What you ideally wanted last year was a concentrated portfolio of large companies, in one sector, in one region and one currency (US large tech).

So, should we throw our golden rules in the bin?

Are we entering a new paradigm where a few big companies will dominate forever?

We don’t think so, as the evidence from history suggests this is rarely the case.

Table one shows the current top 10 stocks in the S&P 500, along with the top performers at various times in the past. (8) Those in bold text show the companies that remain in the top 10 today.

| 2023 | 2010 | 2000 | 1990 | 1980 |

|---|---|---|---|---|

| Apple | Exxon Mobil | General Electric | IBM | IBM |

| Microsoft | Apple | Exxon Mobil | Exxon | AT&T |

| Amazon | Microsoft | Pfizer | General Electric | Exxon |

| Nvidia | Berkshire Hathaway | Citigroup | Philip Morris | Standard Oil, Indiana |

| Alphabet | General Electric | Cisco | Royal Dutch Petrol | Schlumberger |

| Tesla | Walmart | Walmart | Bristol-Myers | Shell Oil |

| Meta | Microsoft | Merck & Co | Mobil Corp | |

| Berkshire Hathaway | Chevron | AIG | Walmart | Standard Oil of Cal |

| Exxon Mobil | IBM | Merck & Co | AT&T | Atlantic Richfield |

| UnitedHealth | Procter & Gamble | Intel | Coca Cola | General Electric |

Source: S&P 500 Dow Jones / awealthofcommonsense.com

Looking back at 2010, five of the top 10 are the same as now, but of those at the top in 2000, only two remain. Of the top 10s from 1990 and 1980, only Exxon remains.

Where are General Electric, AT&T, or IBM today? These were massive incumbents in industries with huge barriers to entry. Where are the likes of Kodak or Blockbuster Video?

Capitalism works. New companies will produce new products and displace the old. Inefficient companies will go bust. Unfortunately, it’s very difficult to know in advance which companies will be which!

That’s why we believe that our golden rules continue to be as relevant today as they have been in the past. By looking for evidence and ignoring stories, by diversifying portfolios and not trying to be too clever, we think we can avoid making the same mistakes that many investors have made, over and over again.

This article is intended as an informative piece and does not constitute a solicitation of investment advice.

Past performance is for illustrative purposes only and cannot be guaranteed to apply in the future.

To speak with one of our experts, contact us here or call us on 0161 383 3335 or by reaching out to your usual Equilibrium contact.

Sources

(1) Amazon returns LSEG Datastream

(2) Nasdaq returns, FE Analytics in US dollars

(3) LSEG Datastream, total US market

(4) FE Analytics 01/01/2023 to 31/12/2023. Equal weight portfolio of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla, rebalanced quarterly

(5) S&P Dow Jones 01/01/2024

(6) FE Analytics 01/01/2023 to 31/12/2023

(7) LSEG Datastream / Equilibrium Investment Management 01/02/2024

(8) S&P Dow Jones/awealthofcommonsense.com