Mark Barlow

Mark Barlow

Trust forms the bedrock of any successful relationship, and this holds true for the bond between banks and their customers. A recent survey conducted by GFT (1) revealed that almost half of British bank customers lack faith in their banks’ ability to assist them in navigating their finances during a recession. However, there is an exception to this trend, and it has garnered rave reviews.

This exceptional establishment is none other than the ‘Bank of Mum & Dad’, which has long been known for its flexibility in extending credit lines and repayment structures. The traditional model involved gradually reducing withdrawals over time, culminating in a potentially substantial financial withdrawal through inheritance.

Does this sound familiar? Is this truly the most advantageous method of making withdrawals? Is it not an outdated approach to running a ‘Bank’?

According to The Times, parents typically authorise withdrawals amounting to £202,660 throughout their child’s formative years until they turn 18. In later years, parents may also assist with university expenses and house deposits before witnessing a reduction in withdrawals as their investment begins to bear fruit and becomes self-sufficient.

As the withdrawal rate from the Bank of Mum and Dad dwindles, the financial focus shifts towards retirement. At Equilibrium, this phase assumes great significance as the focus transitions from accumulation to decumulation. Regular meetings with your financial planner to forecast cash flow can breathe life into your retirement plans and instil confidence in your financial future.

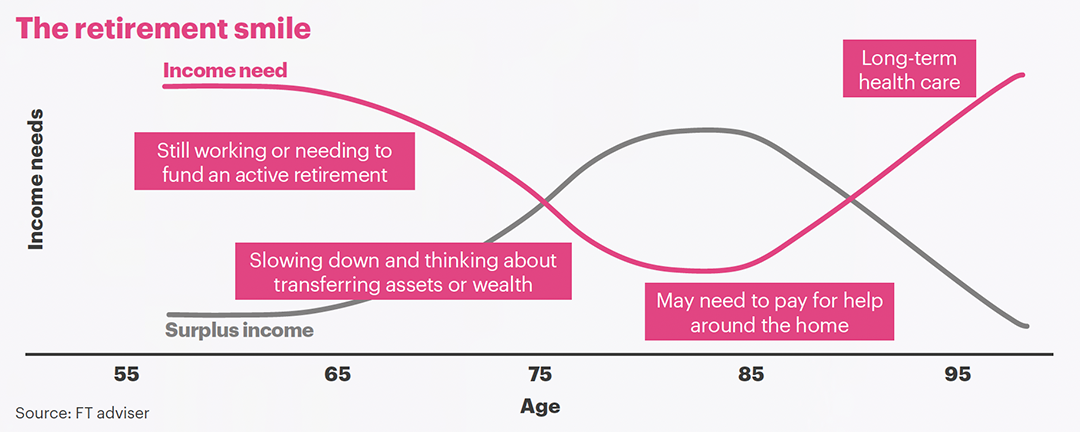

Chartered Financial Planner, Ben Harrison describes the journey of spending in later life as the ‘retirement smile’. He explains: “In the initial years of retirement, individuals tend to spend more as they check off items from their bucket lists. After a few years, they may choose to slow down, leading to a decrease in expenses.”

It is during this phase of slowing down that you may find yourself accumulating wealth once again. But could this surplus income be put to better use?

The dilemma of childcare

After fulfilling their role as the CEO of the Bank of Mum and Dad and settling into retirement, parents witness their children flourish in various aspects of life, be it their careers, relationships, or becoming parents themselves.

The joy of being a grandparent is a magical experience as you bask in the pleasures of retirement.

However, it is at this juncture that your children may require your assistance more than ever.

Every family is unique, but the average UK family now consists of 1.7 children, 1.4 parents, and half a dog (2), all of whom require careful budgeting.

According to data from the National Vital Statistics System, the average interval between the birth of two children is between two and two-and-a-half years, resulting in significant financial outlays during the early years. Let’s examine one of the most substantial costs that families face – childcare.

The cost of childcare

According to the Coram Childcare Survey (2023), the annual childcare cost of 50 hours a week in a nursery setting for a child under two is £14,836, with only a marginal increase from the age of two. (3)

For a single parent with two children earning the UK average net wage of £26,735 (4), the cost of childcare would surpass their take-home salary. Even covering childcare expenses for a single child would be a challenge after paying household bills.

A report by the charity ‘Pregnant Then Screwed’ revealed that one in three families relying on formal childcare resort to some form of debt to meet these costs. Additionally, over three-quarters of mothers (76%) paying for childcare believe that it no longer makes financial sense for them to work. However, for parents who choose to give up work, this decision comes at a cost both professionally and personally.

Christine Morris, a long-standing client of Equilibrium and a mother of six and grandmother of twelve, understands the financial burden of childcare all too well. After a few years of settling into retirement, Christine became aware of her surplus income during a cashflow planning meeting with her Financial Planner, Tim Latham. It had never occurred to her that this surplus could have a profound impact on her family until Tim presented the myriad of opportunities this could provide for Christine and her family.

After engaging in thought-provoking conversations, Christine discovered that her daughter Vanessa was struggling with the cost of childcare after giving birth to her daughter Paige six months earlier.

“I spoke to all my children, and it became evident that Vanessa was torn between returning to work full-time and covering childcare expenses. We agreed to assist with the cost of childcare for a few years, and the difference it has made has been truly remarkable.”

Vanessa initially returned to work part-time at a large accountancy firm but thanks to the additional financial support for childcare, she was able to establish her own company Morris Accountancy Services Ltd and now solely works for herself.

“Having this additional support opened up a world of possibilities for me. I now have a tremendous sense of purpose in both my family and professional roles, which has had a profoundly positive impact on my work-life balance.”

This article is intended as an informative piece and should not be construed as advice. To speak with one of our experts, call us on 0161 383 3335.

Sources

- GFT UK Banking Disruption Index

- Mr Men Research

- Coram Family and Childcare 2023: GB

- Office of National Statistics – average mean