Neal Foundly

Neal Foundly

The stock market is not efficient. Despite the trillions of pounds, the supercomputers, armies of analysts and the Nobel Prize winning geniuses that make up the market, prices swing around and often do not reflect the true value of companies.

It should be quite simple. Shareholders participate in the profits of a company after it has paid the government for taxes and paid its lenders interest on its loans. The share price, therefore, should roughly track the net profits of a business. And yet, it doesn’t.

A company’s share price can deviate massively from its expected profits (investors invest for future returns and it is the future profits that count, much more than past profits). This is particularly the case for smaller companies, such as those that we hold in the Equilibrium AIM portfolio, which are not well covered by research analysts and where prices are more sensitive to large buy or sell trades.

Why should this be?

If a crystal ball could predict, for instance, the holidays and airline operator Jet2’s earnings for the upcoming year, it would sadly not be a reliable indicator of share price returns. A key factor is what value investors put on those profits.

What do we mean by that?

The ‘market’ is expecting Jet2 to make 174p of earnings per share (total net profits divided by all the company’s shares) when they report their figures in July 2025.(1)

Now, with Covid out the way and no signs of an imminent recession, many people are understandably wanting to get away for a holiday break and therefore it is reasonable to assume Jet2 might make those profits – they might even beat them. With the share price currently at 1300p, the ‘value’ that investors are putting on these profits is about seven and half times the expected earnings.

i.e. 174p (earnings per share) x 7.5 = 1300p (the share price)

However, what if there was, say, a rumour of a new Covid-type disease developing? Investors may well take a negative view and put a much lower value on the profits. If they put the shares on five times multiple, this would imply the shares would go down to 870p (174p x 5), a fall of 33%.

Remember, Jet2’s profits might still be 174p per share if the rumour is untrue or the outbreak has zero effect on the company, and yet the shares have lost a third of their value.

Thus, knowing what profits a company is going to make is not necessarily going to tell you what the shares are going to do. Of course, over longer time periods there should be a link.

For example, Chart one is a 10-year chart of one of our AIM portfolio holdings, Next 15 Group, a digital marketing company.

It shows the share price in the black line and the expected earnings per share for the year ahead in the orange line (both rebased back to zero 10 years ago). As you can see, the company has had nice, consistent growth in profits over that time, but the shares have fluctuated pretty widely around the earnings line and now stand at a very low level relative both to earnings, and to the price of a couple of years ago.

In the Equilibrium AIM portfolio, there are many examples like this where the share prices are significantly below the expected earnings line, which is why we believe there is plenty of underlying value yet to be realised in the portfolio. There are several reasons why small companies have been left behind, not least the growth in index tracker funds that focus on large stocks.

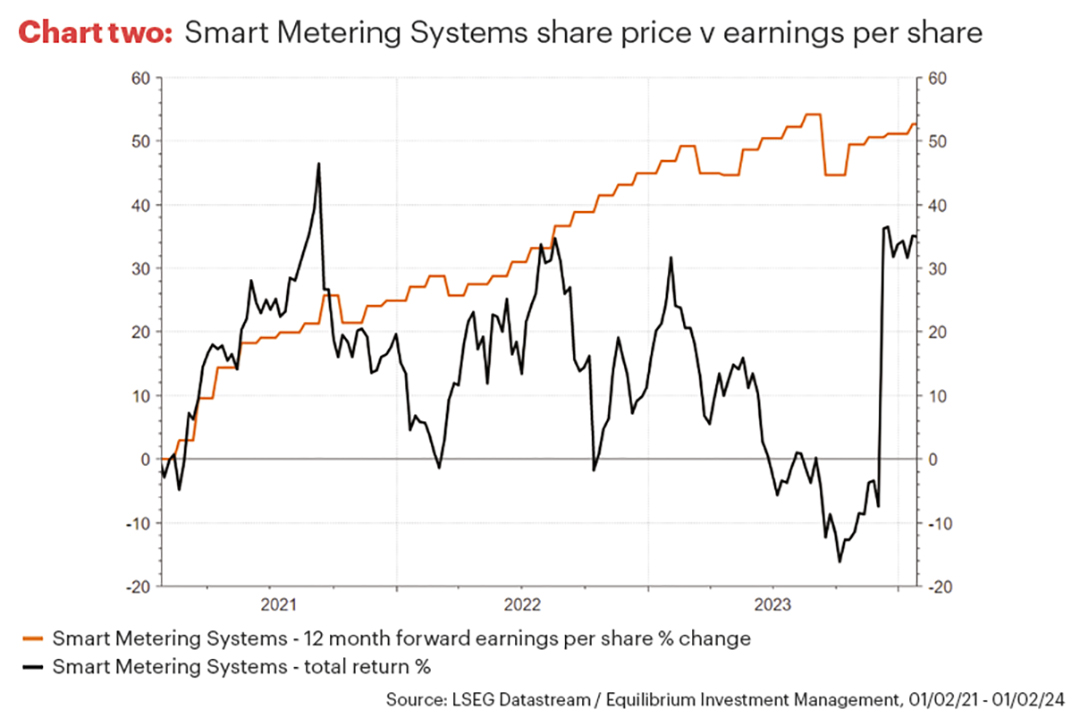

One way in which you can see a rapid closing of the gap between the share price and earnings is when there is a bid for the company.

A recent example of this was the bid by the large private equity company, KKR, for one of the portfolio holdings, Smart Metering Systems. KKR launched an all-cash bid at a 40% premium to the share price in December 2023.

You can see from Chart two that prior to the bid, the share price (black line) had fallen significantly compared to the earnings but the bid, shown as the sharp vertical line at the end of 2023, in large part narrowed this gap.

In total, around 8% of the quoted UK small companies were bid for over the year.(2)

Going forward, we would not be surprised to see this trend continue as prices remain extremely low and as interest rates fall, the cost of borrowing drops, making the opportunities in small companies even more appealing.

Small companies have proven themselves to be the lifeblood of the UK economy, with stronger growth over the long term compared to large companies, and yet they stand at low valuations that provide a great opportunity for investors.

To learn more about our AIM portfolio, contact us here or call us on 0161 383 3335 for a free, no-obligation initial chat.

This article is intended as an informative piece and does not constitute a solicitation of investment advice.

Past performance is for illustrative purposes only and cannot be guaranteed to apply in the future.

Sources

(1) Refinitiv as of 5 February 2023

(2) Bloomberg