Considered Allocation

Asset allocation is key, that’s why we spend a lot of time considering how certain asset classes will react in various scenarios. Graeme Black, Investment Analyst, delves into more detail in this blog.

We spend a lot of time thinking about asset allocation and considering in what scenarios an asset class may make the most gains or protect us if things take a turn for the worse.

Most long-term investment returns are derived from asset allocation rather than simply being in the right fund. If you are invested in the wrong asset class you could find it very difficult to outperform an average fund in the right asset class.

Looking back to Q4 2018 the picture was not too pretty – global equity markets, including the US, were struggling as were most other asset classes. The US central bank (the Federal Reserve) was on ‘auto-pilot’ to continue rate hikes back to more normal levels and 10-year US treasuries were yielding over 3%. If you were heavily invested in risk assets, such as shares, the chances are you were suffering.

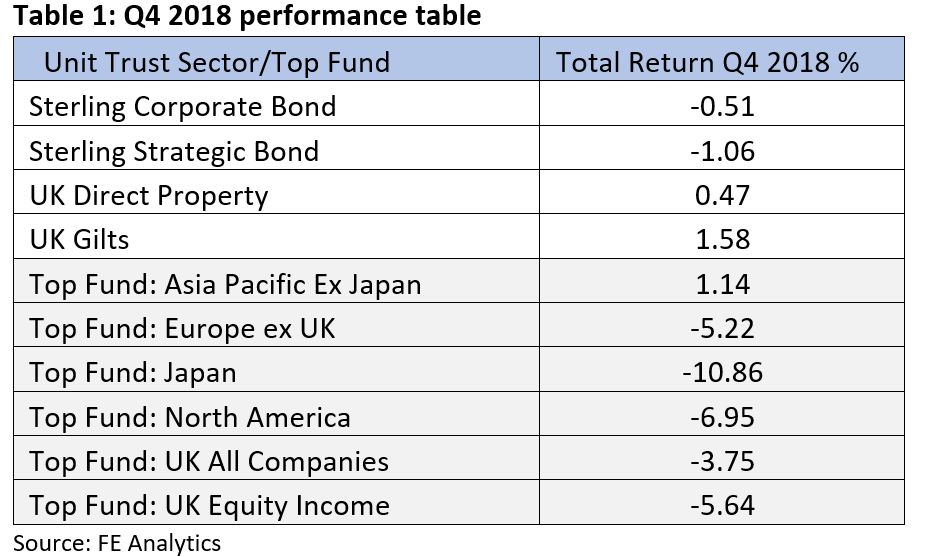

Table one shows the sector average for more defensive fixed interest and property sectors compared to the best returning fund in the more risky equity sectors – only one equity fund (in Asia ex Japan) out of close to 700 was able to beat the sector average for the defensive sectors:

Let’s fast forward six months and the world is very different as equity markets have been on the march, largely recovering the Q4 losses. Central banks, unsettled by global uncertainty, have all but quashed any thoughts of further rate rises which has boosted returns from fixed interest too.

This is all playing out as trade negotiations and Brexit flip-flop, having been on then off and would now appear to be back on again!

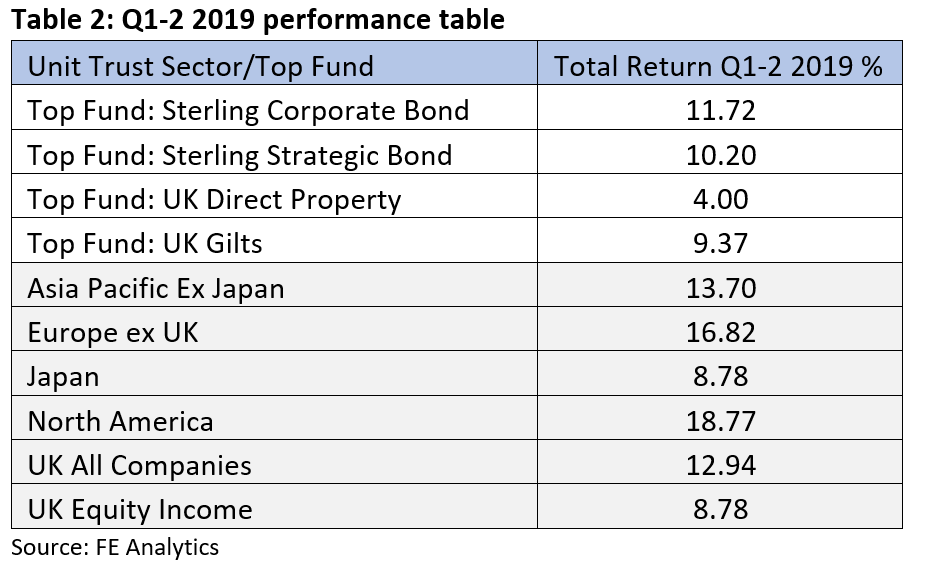

Table two shows a contrasting picture for the first half of 2019 compared to Q3 2018. It shows the best returning funds in the more defensive fixed interest and property sectors compared to the sector averages for the more risky equity sectors – although performing well even the best returning FI funds have struggled to keep up with just the average equity fund in most regions during a strong recovery rally.

Meanwhile in the UK, the well-documented struggles of Neil Woodford have drawn greater focus on investment liquidity. If you haven’t read it, Neal gives an overview of what has happened here.

It’s not a new topic, but recent events have pushed investment liquidity into the spotlight and comments from prominent figures such as Andrew Bailey, the Chief Executive Officer at the Financial Conduct Authority (FCA), and Mark Carney, Governor of the Bank of England, would suggest it is an area that could come under further scrutiny in future.

We are mindful of the liquidity of funds we invest in and of the relative size of our investment in them. Equilibrium’s James Carr has recently shared his ideas on this issue in a recent blog, Size over Substance, which is available to read here.

Property funds have been impacted by liquidity issues in the past – following the EU referendum some property funds were forced to “gate” – effectively stopping any new money coming in or existing investors leaving. Anybody who has bought or sold a house can tell you that property transactions don’t happen overnight!

At the time of writing, we are underweight our strategic allocation for property, as our outlook for this sector is not great. Ongoing retail sector troubles are well covered in national press, and Brexit uncertainty on the economy is also a concern. The risk of potential reforms to the asset class which would negatively impact the types of funds we use means our optimism was eroded further.

Once the decision to reduce this asset class was made we needed to decide what fund(s) were to be sold. This is not a decision to be taken lightly, we take time to research and carry out detailed analysis of funds to ensure we are buying well managed funds with a proven stable approach to investments. Just because an asset class is out of favour it doesn’t mean the funds invested in it turn bad overnight.

As you may expect, the detailed work we put in before and during any investment leads us to have good working relations with all the fund managers we invest with. The fund groups and managers appreciate that asset allocation decisions tend to take precedence when increasing or reducing our exposure to their funds.

Given the implications of relatively large flows in and out of property we felt an open dialogue with the manager was the most effective way to achieve the desired outcome. We certainly didn’t want to try and sell £14m from one fund only to find out that we had inadvertently pushed the fund to a position where they needed to “gate” withdrawals.

By working together with the fund groups through teleconferences we were able to agree the best course of action to reduce our position and achieve best results for our clients.

The recent performance of equity and fixed interest has certainly benefitted our portfolios, but with further uncertainty on the horizon it would be naïve to think these returns are sustainable at this rate going forward. We have been improving our defensive positioning by banking some of the equity gains however with one of our traditional defensive areas (property) out of the picture and some parts of fixed interest looking expensive, the opportunities are scarce.

We are always reviewing our portfolios to ensure we fully understand the investments we make for our clients. We are appreciative of the risks associated with our investments and factor this in when assessing assets classes’ potential for return and loss.

Risk Warning: The content contained in this blog represents the opinions of Equilibrium Investment Management. The commentary in this blog in no way constitutes a solicitation of investment advice. It should not be relied upon in making investment decisions and is intended solely for the entertainment of the reader. Past performance is never a guide to future performance. The value of your investments can fall as well as rise and are not guaranteed. Investors may not get back the amount originally invested.