Mike Deverell

Mike Deverell

Executive summary

- After a brief March wobble, equity markets rebounded sharply in April, with investors largely looking past Middle East risks.

- Supply disruption in oil, gas and fertiliser could keep energy and food prices higher for longer, making near term interest rate cuts less likely.

- US markets led the bounce, driven by strong big tech earnings linked to AI, but gains were narrow and concentrated in a small number of stocks.

- Some headline profit growth reflects rising valuations of stakes in AI firms recorded as “other income”, highlighting reliance on expectations and the need for diversification.

Concentration and correlation

After a brief wobble during March, stock markets bounced back sharply in April.

Although the conflict in the Middle East is ongoing and the Strait of Hormuz remains all but closed, stocks have decided it’s not something they need to worry about!

There have been rumours that Iran and the US are close to some sort of deal, which would of course be good news. However, it’s worth pointing out that, even if the conflict is resolved quickly, damage has already been done to the global economy.

The production and movements of oil and gas around the world will take a long time to get back to normal, meaning energy prices could stay high for some time. In our view, it seems likely that higher fertiliser prices could have a knock-on effect on food prices which could last even longer.

As a result, higher inflation is likely, meaning interest rates probably won’t be cut any time soon. However, as we said in last month’s quarterly report (Quarterly investment report – April 2026 | Equilibrium), this doesn’t mean we’re in for another 2022 situation. In our view, it seems likely that inflation could be a bit higher but not double digit, and we think rates are more likely to stay around current levels rather than go up sharply.

Still, whilst the bond market has digested this view and adjusted accordingly, stock markets don’t seem to care!

US exceptionalism returns

In particular, US stocks have bounced back strongly after a weak start to 2026. As we’ve seen plenty of times in the past few years, it is big tech leading the way.

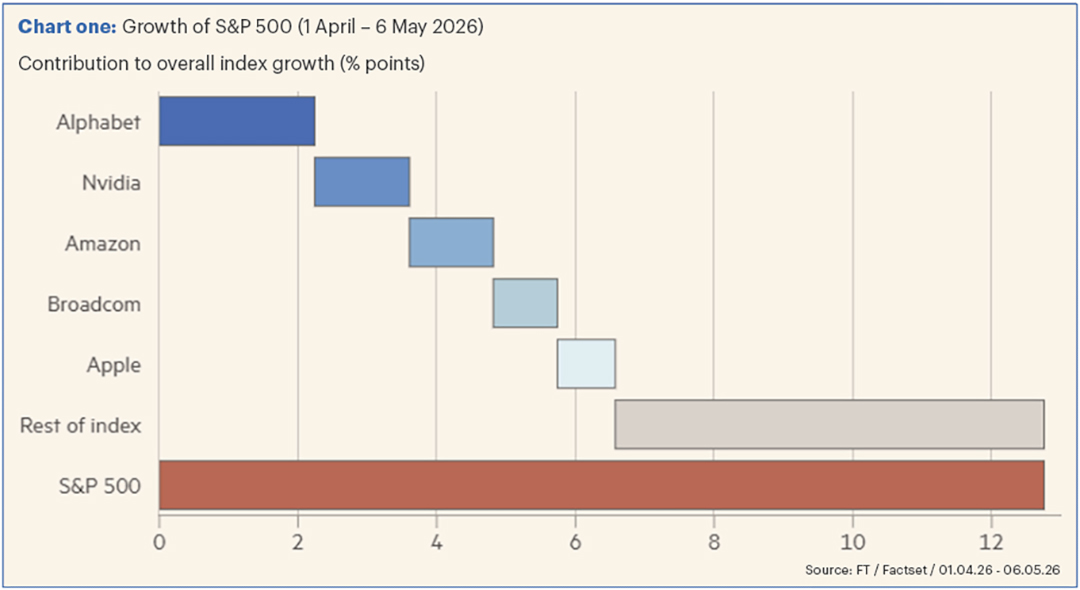

As Chart one shows, the S&P 500 in the US gained over 12% from 1 April to 6 May. But the gains were quite narrow, with about half of this rise accounted for by the share price movements of just five stocks.

The reason these stocks have done so well is all about earnings growth.

The profits of these companies are going up fast, largely driven by artificial intelligence (AI). In the first quarter of this year, the earnings of the S&P 500 grew by over 27% compared to quarter one of last year (Source: Factset).

Within that, the so-called Magnificent Seven big tech stocks saw their earnings increase by over 60% compared to a year earlier!

It seems AI doesn’t care about oil. This is slightly strange, because one of the big costs of AI is energy, where data centres and chip manufacturers require vast amounts of energy (and water). Higher energy prices as a result of the Middle East conflict could still impact on profits.

Despite this concern, these are still impressive growth figures.

All is not as it seems?

Whilst the earnings growth figures are impressive, it is important to understand exactly what this represents.

Profits usually go up because of a combination of increased revenue and/or reduced costs.

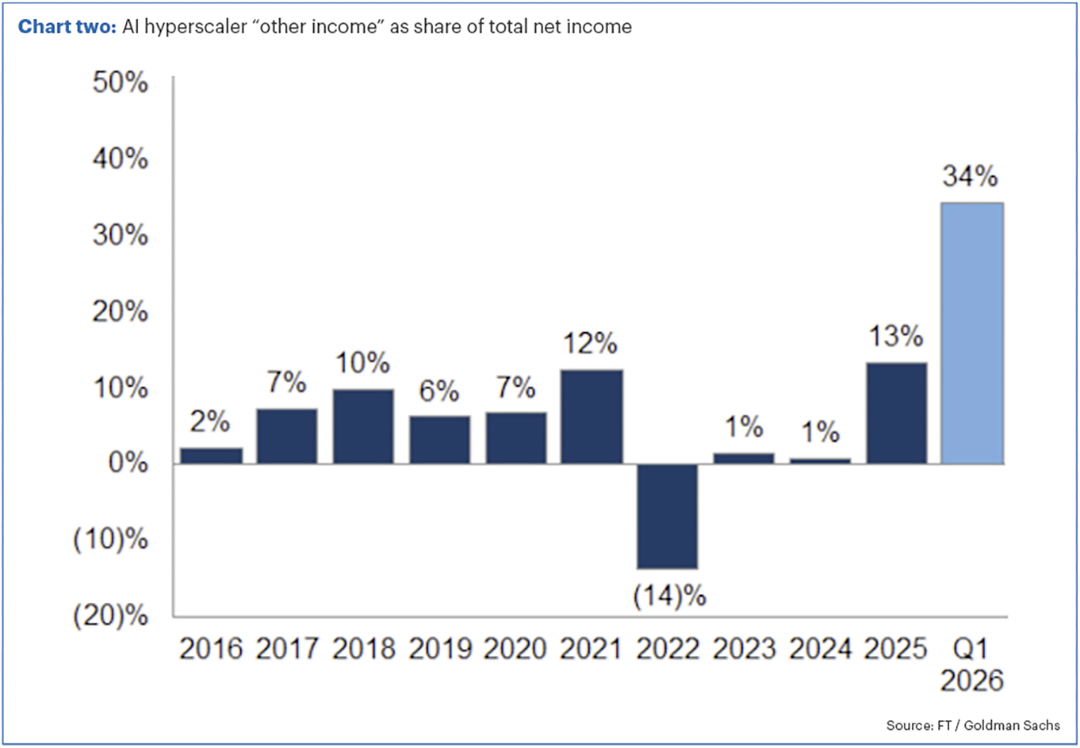

But a recent article from the FT Alphaville team highlighted that in the most recent set of figures, a much larger proportion than usual of profit is being described as “other income” in accounts.

Chart two shows that in the big tech “hyperscalers”, this “other income” accounted for over a third of total net income in the current quarter, far higher than the usual proportion.

So, what’s going on?

Well according to the Alphaville team, it isn’t actually “income” in the traditional sense.

This figure has been largely driven by an increase in value of the stakes that big technology companies (known as the ‘AI whales’) hold in AI firms.

For example, both Alphabet (Google) and Amazon own big stakes in Anthropic (makers of Claude), one of the leading AI companies. According to Pitchbook, Anthropic was worth $183bn in September but is worth $380bn today. The Financial Times has also recently reported that the company is expected to be valued at $900bn in the next fund-raising this summer, six times the valuation a year ago! (FT, 8 May 2026).

In the US, companies have to report this type of capital gain as income (and pay tax on it). In reality, the increase in the share price of a holdings doesn’t really mean anything much until it is sold.

So “other income” in this instance doesn’t so much reflect greater revenue, but a “notional” capital gain.

Again, this highlights how interconnected the AI ecosystem is, with firms such as Anthropic and OpenAI (makers of ChatGPT) shaping much of the momentum in the tech sector.

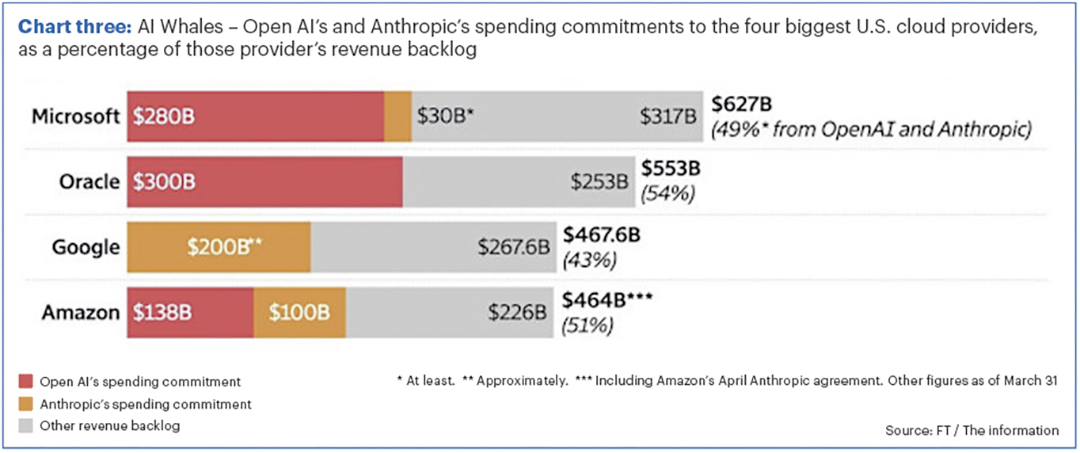

The same article shows how much the spending commitments of those two firms are boosting expected revenue of the leading cloud computing firms.

Spending commitments by OpenAI and Anthropic represents almost half of the expected revenue of some of these providers, as illustrated in Chart three.

Again, this is fine as long as expectations are met. But it does give some cause for concern about how much stock markets are dependent on the performance of a very small number of companies.

Again, this is fine as long as expectations are met. But it does give some cause for concern about how much stock markets are dependent on the performance of a very small number of companies.

Emerging technology

It is not just US stocks that have been boosted by the AI trend.

Some of the companies which have made the biggest gains as a result of AI, are US semiconductor stocks such as Nvidia and Broadcom.

However, whilst those two firms design microchips, they don’t actually manufacture them.

The chips themselves are made largely by Taiwan Semiconductor Manufacturing Corporation (TSMC). It is a very specialist operation and is very difficult for other firms to develop the same capabilities.

Shares in TSMC have done extremely well, and the company is now by far the biggest in the emerging market universe, representing over 13% of the MSCI Emerging Market Index.

Other chip manufacturers have also profited, with Samsung now representing over 5% of the index, and fellow Korean company SK Hynix not far behind. (Source: FT / Bloomberg / MSCI)

In the past, we’ve often had quite a large holding in emerging markets, which has historically not just been a source of high potential returns, but also provided diversification compared to developed market stocks.

However, with the index becoming more concentrated and increasingly linked to the AI trade, the risks are rising and we think the correlation with the US market in particular might be higher in future.

That doesn’t mean we’re avoiding emerging markets, or indeed the US. It is just another risk to be aware of in portfolios.

One of our core beliefs is in diversification – to smooth the investment journey, we should be very widely diversified. With stock market indices becoming more concentrated, we need to work that bit harder to hedge the risks and find assets that will act differently to our equity holdings.

Past performance is for illustrative purposes only and cannot be guaranteed to apply in the future.

This newsletter is intended as an information piece and does not constitute investment advice.

If you have any further questions, please don’t hesitate to get in touch with us on 0161 486 2250 or reach out to your usual Equilibrium contact.

New to Equilibrium? Call 0161 383 3335 for a free, no-obligation chat or contact us here.