Mike Deverell

Mike Deverell

Trillionaires and turning points

Executive summary

- Major technology companies may be entering a new phase of equity issuance, driven by the rising cost of AI infrastructure and data centres.

- For more than two decades, share buybacks have reduced the supply of equities and helped support markets, but that tailwind may now be weakening.

- A potential US and Iran deal could ease pressure on oil and commodity markets, although disruption may take time to unwind.

- Geopolitical uncertainty remains a key market risk, making diversification and the ability to react quickly especially important.

With the recent initial public offering (IPO) of SpaceX, Elon Musk has become the world’s first trillionaire.

With wealth of around $1.1 trillion according to Forbes (as of 15 June), Musk has more money than the poorest 4 billion people on the planet combined, or around half the world’s population.

The world’s second richest person is Larry Page who Forbes reckon is worth $294bn. The gap between Page and Musk in terms of wealth is around £800bn, meaning we are all closer in wealth to the world’s second richest man than he is to the richest!

Of course, much of this is currently “paper wealth”. Musk still owns most of SpaceX, with less than 5% of the company being listed on the stock exchange so far. The amount raised in the IPO was a “mere” $75bn, although at the time of writing the shares have since gone up by around 20% in the first day of trading.

The SpaceX IPO may not even be the biggest equity raise this year, at least in terms of the value of the shares actually sold.

The two big artificial intelligence (AI) developers, OpenAI (makers of ChatGPT) and Anthropic (who produce Claude) have begun the IPO process and may well come to market this year.

Like SpaceX, both could also be valued close to the $1 trillion mark, although how much equity they actually decide to raise is yet to be seen.

Not just IPOs

Companies don’t just raise money via IPOs. Companies that are already listed can also raise money by selling equity.

Alphabet (owners of Google) have announced that they will carry out an equity raise in the coming months, expected to be around $85bn.

This would in essence be bigger in terms of money raised than SpaceX.

Meta (Facebook and Instagram) are also reportedly considering raising tens of billions in equity, having issued $30bn of debt in the forms of bonds last year.

As the AI race accelerates, the big tech firms are spending more and more money building the infrastructure behind it, including huge amounts spent on building data centres.

Previously, these firms were seen as “asset light” businesses. They generated great profit margins as they didn’t have the same sort of overheads as (for example) a manufacturing business which needs to run factories and constantly invest in new equipment.

That means that big tech companies have historically had way more cash than they knew what to do with, and very little debt.

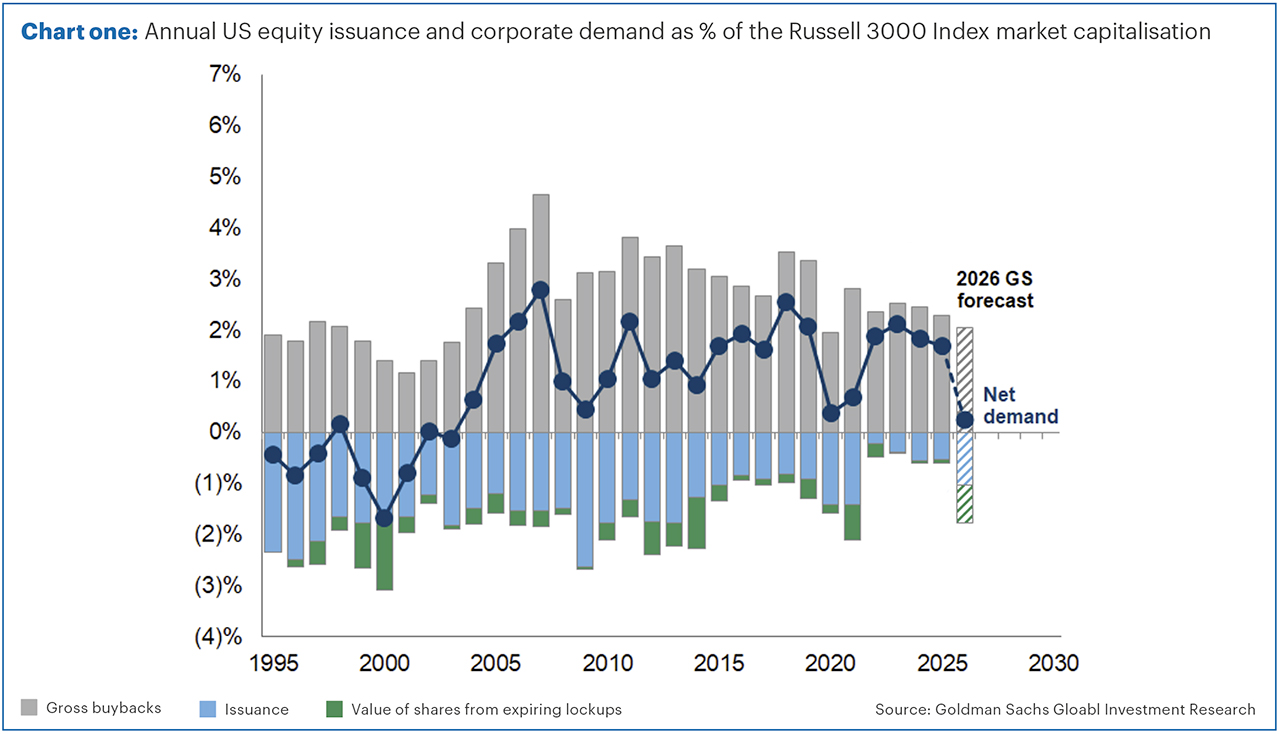

A lot of the time, the companies were actually returning cash to shareholders by carrying out share buybacks. In the US in particular, this was often more tax efficient than paying dividends.

What it meant was that the number of shares in issue of certain companies has been falling over the years.

In fact, over the last 20 years or more, the value of shares bought back in the US has more than exceeded the amount being issued.

Chart one shows the number of buybacks and equity issuance, as a % of the US market over time.

It also shows the net position between the supply and demand. In essence, the supply of equities has generally been shrinking since the early 2000s. This has likely caused a tailwind for stocks as falling supply and rising demand tend to push them higher.

But as the chart shows, this trend looks like it’s about to change.

Many companies have now stopped or reduced buybacks and the big tech stocks have much less cash on balance sheets than they used to. With all this new issuance coming to market, supply may be about to exceed demand for the first time in more than two decades.

This doesn’t necessarily mean share prices will fall. If the companies continue to grow their profits at current rates, then we still think it likely markets will go up over the long term.

It’s just worth noting that one of the tailwinds helping markets has now turned into a headwind.

Do we finally have a deal?

At the time of writing (Monday 15 June), US president Donald Trump has announced they have made a deal with the Iranians.

This will (apparently) involve an end to all conflict and the re-opening of the Strait of Hormuz, the sea channel which enters the Persian Gulf.

The two sides will then begin a period of negotiation covering things like Iran’s nuclear ambitions before finalising any agreements.

It is important to wait and see whether this deal holds and if ships start entering and exiting the Gulf again. According to CNN, Trump has declared the conflict is about to end around 38 times over the past couple of months!

But assuming the deal holds, this is very welcome. It should allow oil, natural gas and other commodities (including chemical and fertiliser) to be exported from the Middle East much more easily than is currently the case.

The oil price has fallen sharply on the news. However, what we don’t know, is how long things take to get back to something approaching “normal”. The supply of oil and gas will likely remain partially disrupted for several weeks or months, with damage to oil infrastructure, and with some oil fields and refineries “offline” therefore it may take a while to bring them all back online again.

So, whilst it appears the worst-case scenarios appear to have been avoided, we also still expect inflation to continue to move moderately higher in the short term based on what has already happened.

Central banks may be able to look through this and keep interest rates on hold, rather than having to hike rates as seemed likely a few weeks ago. However, they are no longer thinking of cutting any time soon, as they were expected to do before the conflict began.

As we’ve discussed several times recently, we live in an increasingly uncertain world and geopolitics is a big part of that instability. This can make investing more difficult, since markets can react sharply to geopolitical events in either direction!

From an investment management perspective, the best defences against this are diversification – holding a variety of assets that perform differently to stock markets – and speed of reaction. This gives us the ability to profit from volatility by buying the dips and selling the rallies.

Past performance is for illustrative purposes only and cannot be guaranteed to apply in the future.

This newsletter is intended as an information piece and does not constitute investment advice.

If you have any further questions, please don’t hesitate to get in touch with us on 0161 486 2250 or reach out to your usual Equilibrium contact.

New to Equilibrium? Call 0161 383 3335 for a free, no-obligation chat or contact us here.