Neal Foundly

Neal Foundly

Almost constantly throughout my nearly four decades in investments, commentators have complained the markets “have never been so difficult to call” or “the most uncertain they have ever been”.

It’s a bit like TV shows that always declare the next contest “is the toughest challenge yet” – it rarely is, it’s just different. In markets, there are always things to challenge investors, and so we need to constantly adapt to deal with new or changed circumstances.

Who knows what 2026 will throw at us; Venezuela and Greenland have been early out of the blocks, but it is likely that bigger issues for investors will arise as the year unfolds.

As evidence-based investors, we care less about year-ahead outlook forecasts or prognostications in the media than underlying valuations. To remind myself of this, I keep on my desk The Economist Outlook Edition for 2020 which said the “worst-case scenario is that the trade war turns inflationary”.(1) Less than two weeks into the year, China announced the first death from Covid.

Investing is not only about analysing the direct implications of local and global events but also understanding market trends. For example, let’s look at how UK investors have actually traded in recent years to get a handle on what assets might be overbought or oversold. You might think with globalisation that UK investors are small fry, but total assets under management in the UK are still around £10 trillion, which is about 11% of the world’s investment capital – we are still a mid-sized fish!

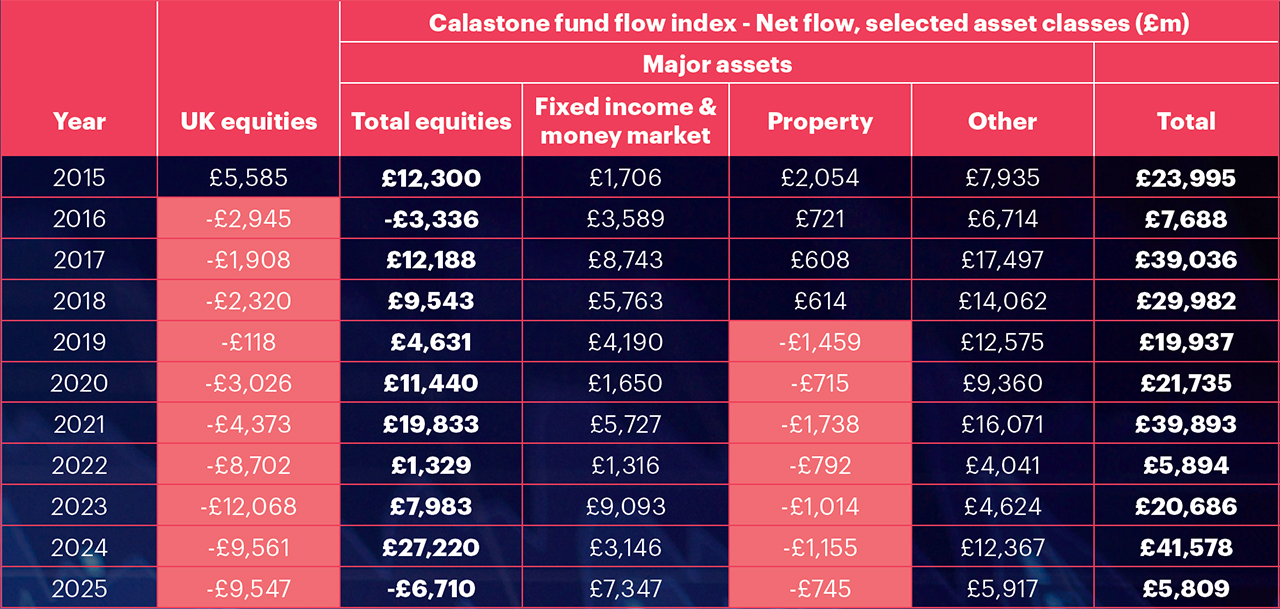

Table one shows the net value of investments (all the purchases minus the sales) by UK investors in and out of the different assets (notable outflows highlighted in pink). A key notable trend has been the ten consecutive years of selling of UK shares.

Table one: Calastone Fund Flow Index – Net Flow, selected asset classes (£m)

There are a multitude of reasons for this, not least the globalisation of capital over the decade, in particular the rise of the US stock market which now constitutes around 70% of the value of all the world’s shares.

To try to stem this outflow, the London Stock Exchange has belatedly tried to reduce the red tape and cost of listing in this country. Equally, the government has struggled to encourage investors to boost holdings in UK shares to emulate overseas pensions that generally have much higher domestic holdings.

We find this interesting as it probably reflects that much of the selling of UK shares has probably been completed now. The UK stock market was around 8% of the value of the global stock market a decade ago and is now down to around 3.5%, less than half the weighting.

A second key takeaway from the table is the seven consecutive years of property investment sales. Again, there are good reasons behind this, not least uncertainty caused by Brexit in 2016; the cooling of the industrial market as demand for distribution warehouses abated in the late 2010s; the significant impact on office demand due to the pandemic in 2020, then followed by the ramp up in interest rates in 2022 which quashed any hope of new (debt-laden) property developments.

Again, this is interesting. For all these reasons, supply has dried up whilst at the same time the economy has continued to grow. Real estate company Knight Frank believes that the supply shortage in London is such that the vacancy rate for quality office space will fall to zero by 2028 and remain there until the end of the decade.(2)

Not necessarily ideas for this week, month or even this year, but this is the sort of real-world evidence we use to inform our decision-making. It is interesting, for example, to reflect on the fact that the UK’s FTSE 100 Index returned nearly 26% in 2025, beating four of the high-flying US Magnificent Seven technology stocks….imagine what it would have done if UK investors were buying too.

Events ebb and flow, and there are times when there are so many changes going on that it is easy to be bamboozled. We seem to lurch from one crisis to another with the occasional ‘polycrisis’ where multiple, interconnected crises occur at the same time.

In the modern world, the word ‘crisis’ usually implies some form of heightened uncertainty or potential disaster. The Greek origin of the word is ‘krisis’ which means a point of decision or judgement. This is an altogether more measured approach we prefer to take; a calm assessment of the facts and rational decisions will hopefully carry us through the many more ‘toughest challenges’ ahead.

This article is intended as an information piece and does not constitute investment advice.

(1) The Economist, The World in 2020

(2) Financial Times, “London office shortage forces big companies to stay put”, 6 January 2026

If you have any further questions, please don’t hesitate to get in touch with us on 0161 486 2250 or reach out to your usual Equilibrium contact.

New to Equilibrium? Call 0161 383 3335 for a free, no-obligation chat or contact us here.